The S-Corp Election:

Cut Self-Employment Tax by $10K–$30K+/Year

The single most impactful tax election for self-employed professionals, 1099 contractors, and business owners earning $50K+ in net profit — and the most commonly missed opportunity in small business tax planning.

What Is an S-Corp Election?

An S-Corp election is a tax classification — filed on IRS Form 2553 — that allows a business owner to split their income into two categories: a reasonable salary (subject to payroll taxes) and shareholder distributions (not subject to self-employment tax). This single election can save self-employed professionals $10,000–$30,000+ per year in Social Security and Medicare taxes — legally and without changing how you operate your business.

The S-Corp is not a new type of business entity. It's a federal tax election available to qualifying LLCs and corporations under IRC Subchapter S (§§1361–1379). Your LLC keeps its state-law liability protection. Your day-to-day operations stay the same. The only thing that changes is how the IRS taxes your income — and for most self-employed professionals earning above $50K–$70K in net profit, the savings are substantial.

This guide covers everything: how the S-Corp election works, the reasonable compensation rules the IRS uses to evaluate your salary, the break-even thresholds where the election starts making sense, the ongoing compliance requirements, a detailed case study showing $22,000+ in annual savings for a physician with 1099 income, and the common mistakes that trigger audits. Whether you're a 1099 contractor, locum tenens physician, consultant, or small business owner, this is the most complete S-Corp election guide available — fully updated for 2026, including the permanently extended Section 199A QBI deduction under the OBBBA.

$10K–$30K+

Typical annual SE tax savings for qualifying professionals

15.3%

Self-employment tax rate avoided on distributions above salary

$50K+ Net

Approximate minimum profit threshold where the election makes sense

If you're a physician, consultant, freelancer, or business owner paying self-employment tax on 100% of your net income, you're likely overpaying by thousands of dollars per year. The S-Corp election is the most straightforward, legally established, and widely used strategy to fix this — and it's available to nearly every profitable self-employed individual.

The Self-Employment Tax Trap

Why being self-employed costs 15.3% more than most people realize — and how the S-Corp fixes it.

You leave your W-2 job — or you start picking up 1099 contracts on the side. You earn $200,000. You think: "I'll pay income tax, just like before."

Then your CPA gives you the bad news: "You owe an additional $25,000+ in self-employment tax."

This is the self-employment tax trap. When you're a W-2 employee, your employer pays half of your Social Security and Medicare taxes (7.65%), and the other half (7.65%) is withheld from your paycheck. As a self-employed individual — whether you're a sole proprietor or a single-member LLC — you pay both halves: 15.3% on every dollar of net self-employment income, up to the Social Security wage base ($184,500 in 2026). Above that, you still pay the 2.9% Medicare tax (plus 0.9% Additional Medicare Tax on income above $200,000/$250,000 MFJ).

"Wait — I'm paying 15.3% in tax on top of my income tax? On every dollar?" — Yes. Unless you elect S-Corp status.

Here's what the self-employment tax looks like on real income levels:

| Net Self-Employment Income | SE Tax (Sole Prop / LLC) | Approx. Effective SE Rate |

|---|---|---|

| $75,000 | $10,597 | 14.1% |

| $100,000 | $14,130 | 14.1% |

| $150,000 | $21,194 | 14.1% |

| $200,000 | $26,532 | 13.3% |

| $250,000 | $29,432 | 11.8% |

| $400,000 | $33,782 | 8.4% |

These are real dollars — paid in addition to your federal and state income taxes. For a physician earning $300,000 in 1099 locum tenens income, the SE tax bill alone is approximately $31,000. That's money that could be in a Solo 401(k), a brokerage account, or paying down debt.

The S-Corp election doesn't eliminate self-employment tax entirely — you still pay it on your reasonable salary. But it eliminates SE tax on every dollar of profit above your salary. That's the mechanism. That's the savings.

The 15.3% Is Not a Deduction — It's a Direct Cash Cost

Many business owners focus on income tax rates and overlook the SE tax entirely. You get to deduct half of the SE tax on your 1040 (the "employer" portion), but you still pay the full 15.3% out of pocket. The S-Corp election is the only way to legally reduce the base on which this tax is calculated without reducing your actual income.

How the S-Corp Election Works

One form. Two income buckets. Thousands in tax savings — every single year.

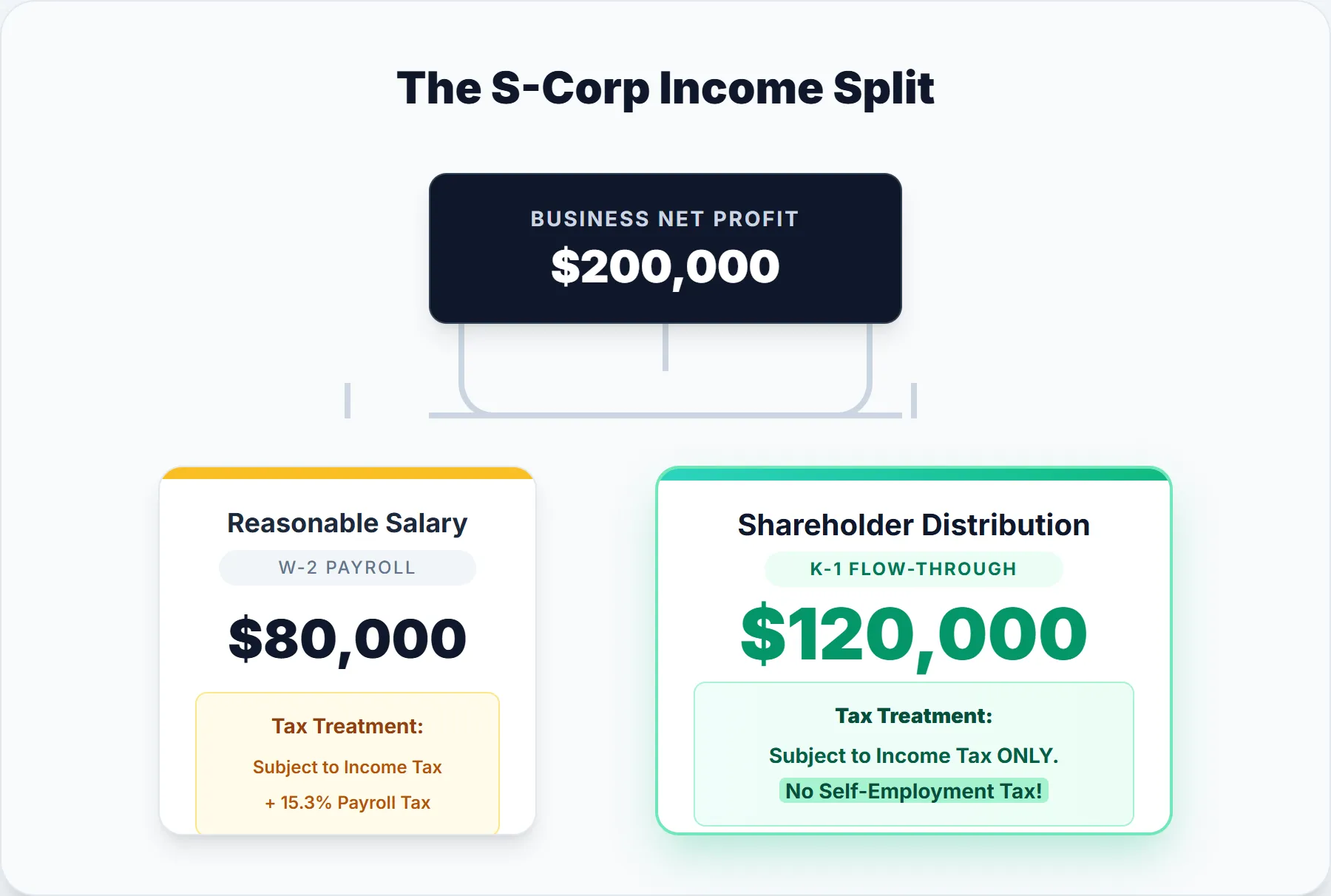

The Core Mechanism: Salary vs. Distributions

The S-Corp election works by splitting your business income into two categories:

Bucket 1: Reasonable Salary (W-2)

This is the amount you pay yourself as an employee of the S-Corp, processed through payroll. It's subject to both income tax and payroll taxes (Social Security + Medicare) — the same 15.3% split between employee and employer.

Tax Treatment

Federal income tax + 7.65% employee FICA + 7.65% employer FICA

Bucket 2: Shareholder Distributions (K-1)

Everything above your salary flows through to you as a shareholder distribution on Schedule K-1. This is subject to income tax only — no self-employment tax, no FICA, no payroll tax.

Tax Treatment

Federal income tax ONLY — no SE tax

The total amount you take home doesn't change. You still earn the same income and pay the same income tax. The only difference is that the profit above your salary is no longer subject to the 15.3% self-employment tax. That's the entire strategy.

S-Corp Election at a Glance

The Tax Math: A Simple Example

Let's walk through a concrete example. Dr. James is a locum tenens physician earning $250,000 in 1099 income with $20,000 in business expenses — so $230,000 in net self-employment income.

| Without S-Corp (Sole Prop) | With S-Corp Election | |

|---|---|---|

| Net Business Income | $230,000 | $230,000 |

| Reasonable Salary (W-2) | N/A | $120,000 |

| Shareholder Distribution | N/A | $110,000 |

| Income Subject to SE/FICA Tax | $230,000 (100%) | $120,000 (salary only) |

| Approx. SE / Payroll Tax | $29,000 | $18,360 |

| Annual SE Tax Savings | — | $10,640 |

| QBI Deduction (§199A) | Up to $46,000 (20% of $230K) | Up to $22,000 (20% of $110K distribution) |

The QBI Tradeoff Is Real

Notice the QBI deduction line. Under Section 199A, you get a 20% deduction on qualified business income — but your W-2 salary from the S-Corp does not count as QBI. Only the pass-through profit (the $110,000 distribution) qualifies.

This creates a tension: a higher salary saves more SE tax but reduces QBI. A lower salary maximizes QBI but risks IRS scrutiny. This is exactly why reasonable compensation analysis is not a DIY exercise. The optimal salary balances both variables. We model this for every client.

The S-Corp election doesn't change your income tax rate. It only changes the self-employment/payroll tax calculation. You'll still pay federal and state income tax on the full $230,000 — but you'll save $10,640+ per year on the SE tax portion. Over 10 years, that's over $100,000 in cumulative savings from a single election. Use our S-Corp Calculator to model your specific savings.

Want Us to Run the Numbers for Your Situation?

We'll model your self-employment tax savings, determine the optimal reasonable salary, factor in the QBI deduction impact, and tell you whether the S-Corp election makes sense for your specific situation — all in a 30-minute call.

Book a Free ConsultationNo obligation • Takes 30 minutes • Done over the phone

S-Corp Benefits: What Actually Changes

The advantages of an S-corp in plain English — and the misconceptions that get owners in trouble.

Most high-income business owners don't have a tax problem — they have a structure problem. An S-Corp doesn't magically create savings. It changes how income is classified and which dollars are subject to payroll taxes. When profits are consistent and the structure is implemented correctly, the S-Corp election is one of the highest-leverage (and least flashy) tax decisions available. When implemented too early, or for the wrong reasons, it often just adds complexity.

Here's an honest scorecard of what the election actually changes:

The Real Benefits

- Payroll tax savings on the portion of profit taken as distributions — typically $10K+/year above the break-even threshold

- Clean separation between salary and distributions, which supports retirement-plan and fringe-benefit strategies

- More structured compensation, bookkeeping, and reporting — the discipline that makes proactive planning possible

- Access to Accountable Plan reimbursements and Solo 401(k) employer contributions built on your W-2 wage base

The Real Tradeoffs

- Payroll is mandatory — with quarterly filings, W-2s, and admin work

- An additional tax return (Form 1120-S) and $2K–$5K/year in compliance costs

- Reasonable compensation rules must be followed and documented

- Rarely beneficial at low or inconsistent profit levels

Common Misconceptions About S-Corp Advantages

"An S-Corp always saves taxes."

Not true. If profits are low or inconsistent, admin costs and payroll can outweigh any benefit.

"I can just pay myself $40K and distribute the rest."

This is one of the fastest ways to turn a good plan into an audit problem. Reasonable compensation matters — see the next section.

"An S-Corp lets me deduct more expenses."

Entity type doesn't create deductions. Documentation and business purpose do.

"I should elect S-Corp status as soon as I form an LLC."

Often premature. Many owners wait until profits stabilize above the break-even threshold before electing S status.

The S-Corp election tends to work well when profits are consistent beyond a market-rate owner salary, the owner actively works in the business, clean bookkeeping and payroll discipline already exist, and the business is past the startup phase. It tends to fail when profits are low or volatile, the owner wants to avoid payroll and admin complexity, the activity is primarily passive investment income, or the goal is tax savings without structure or documentation.

Wondering how the S-Corp stacks up against your current structure? See our sole proprietorship vs. S-Corp comparison and the full LLC vs. S-Corp guide for the entity-selection decision.

Reasonable Compensation: The Key to Compliance

The IRS doesn't care that you elected S-Corp status. They care about how much you pay yourself — and whether it's defensible.

Reasonable compensation is the single most audited aspect of S-Corp taxation. The IRS knows that S-Corp owners have an incentive to set their salary as low as possible (to maximize SE tax savings on distributions). They actively look for it — and they have a strong track record of winning in Tax Court when owners can't justify their salary.

There is no bright-line rule, no magic formula, and no safe harbor percentage. The IRS uses a facts-and-circumstances test based on factors established in case law.

Training and Experience

What education, certifications, and years of experience do you bring? A board-certified surgeon and a first-year freelance writer have very different market value. The IRS compares your background to what someone with similar qualifications would earn as an employee.

Duties and Responsibilities

What do you actually do for the business? If you perform all services — marketing, client work, billing, management — you'd need to pay an employee more to replace you than if you only handle one function. The broader your role, the higher the justifiable salary.

Time and Effort Devoted

How many hours per week do you work in the business? A 1099 consultant working 50 hours a week justifies a higher salary than one working 15 hours. The IRS will compare the hours you work to a full-time employee in a similar role.

Comparable Salaries in Your Industry and Location

MOST IMPORTANTThis is the factor the IRS weighs most heavily. What would a similarly qualified person earn as an employee performing the same services in the same geographic area? We use Bureau of Labor Statistics (BLS) data, Robert Half salary guides, Medscape physician compensation surveys, and industry-specific benchmarks to document this. If a marketing consultant in Chicago would earn $95,000 as an employee, paying yourself $40,000 as the S-Corp owner won't hold up.

Company Profitability and Distribution History

If the S-Corp is distributing large profits while paying a tiny salary, that's a red flag. The IRS looks at the ratio of salary to total compensation. A company earning $500,000 with a $40,000 salary and $460,000 in distributions will attract scrutiny. The salary should reflect a reasonable portion of the income generated by the owner's personal services.

The "60/40 rule" you see on the internet is a myth. There is no IRS-approved formula that says "pay yourself 60% as salary and take 40% as distributions." The IRS has explicitly rejected percentage-based approaches. Reasonable compensation must be based on what you would earn as an employee — period. Some owners' reasonable salary is 40% of profit. Others' is 80%. It depends entirely on the facts.

How We Set Reasonable Compensation at Taxstra

For every S-Corp client, we prepare a documented reasonable compensation analysis that we keep on file. This is your audit defense. It includes:

Median and percentile wage data for your specific occupation code and metropolitan area

Robert Half, Medscape, MGMA, and profession-specific compensation surveys

Written memo addressing each IRS factor with supporting data specific to your situation

Balancing SE tax savings against the Section 199A deduction to find the optimal salary

If your CPA set your S-Corp salary without conducting a formal compensation study, you're exposed. "We just picked a number" is not a defense in Tax Court. The reasonable compensation analysis is the single most important document in your S-Corp compliance file. Read our deep dive on S-Corp reasonable salary rules — including the three valuation approaches, safe ranges by profession, and documentation requirements — for the full picture.

When to Elect S-Corp Status

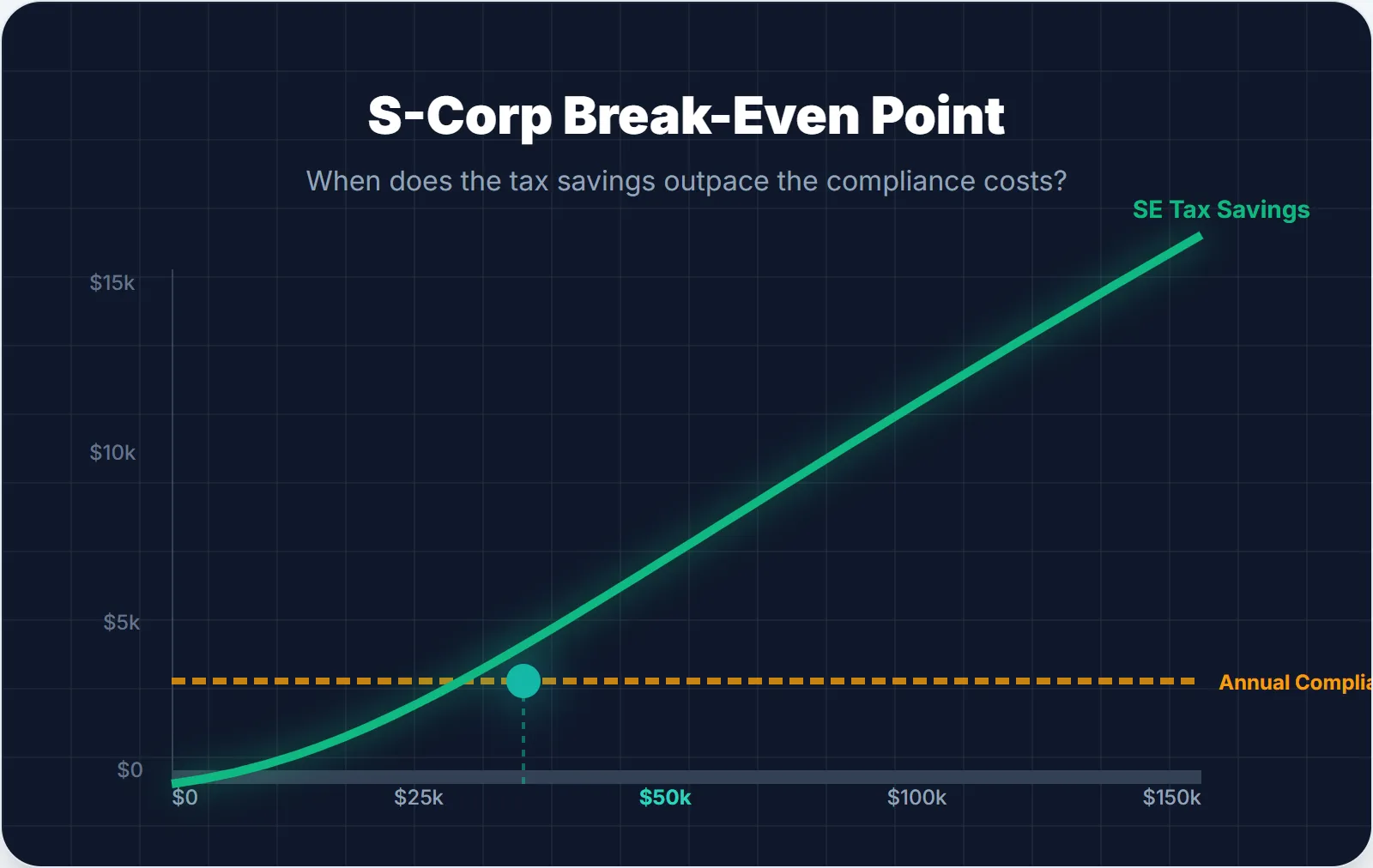

Timing, profit thresholds, and the break-even analysis that determines whether the election is worth it.

The Break-Even Analysis

The S-Corp election is not free. It comes with ongoing compliance costs that a sole proprietorship or disregarded LLC doesn't have:

| Compliance Item | Typical Annual Cost | Notes |

|---|---|---|

| Payroll Processing | $500–$1,500 | ADP or similar — depends on frequency |

| Form 1120-S Tax Return | $1,000–$2,500 | Separate business return due March 15 |

| Bookkeeping (additional) | $500–$1,500 | Payroll journal entries, distributions tracking |

| Reasonable Comp Study | $300–$800 | Annual documentation (included in Taxstra plans) |

| State-Level Compliance | $0–$1,500 | Varies — some states charge S-Corp franchise taxes |

| Total Annual Overhead | $2,000–$5,000+ | Must be offset by SE tax savings |

For the S-Corp election to make financial sense, the SE tax savings on your distributions must exceed these compliance costs. Here's the general break-even math:

Break-Even by Net Profit Level

This is a general guideline. Your specific break-even depends on state taxes, your reasonable salary, QBI deduction impact, and compliance costs. We model this precisely for every client before recommending the election.

Critical Deadlines

Missing the S-Corp election deadline is one of the most common and costly mistakes we see. Here are the deadlines you need to know:

New Entity: Within 75 Days of Formation

If you form a new LLC and want S-Corp treatment from day one, you must file Form 2553 within 75 days of formation. Don't wait — this is the easiest deadline to hit and the one most frequently missed because owners don't realize the clock is ticking.

File Form 2553 immediately after forming your LLC or corporation

Existing Entity: By March 15

For an existing LLC or corporation that wants to elect S-Corp status for the current tax year, the deadline is March 15. For example, to be treated as an S-Corp for all of 2026, Form 2553 must be filed by March 15, 2026. Check the full tax deadline calendar for all key dates.

Calendar-year taxpayers — file by March 15 for the current tax year

Late Election Relief: Rev. Proc. 2013-30

Missed the deadline? You may still be eligible for late election relief if you had reasonable cause for the delay and intended to be treated as an S-Corp. The IRS grants late elections under Revenue Procedure 2013-30 — but only if filed within 3 years and 75 days of the intended effective date. We file late elections regularly for new clients who missed the window.

Up to 3 years and 75 days after intended effective date

How to File Form 2553, Step by Step

Mechanically, the S-Corp election is one form: Form 2553. You keep your existing LLC, your name, and your EIN — the form simply tells the IRS to tax the same entity differently. Here's what the form actually requires:

- Part I — Election Information: Entity name, EIN, address, date incorporated or formed, state of formation, and the tax year the election should take effect.

- Shareholder consent: Every shareholder must sign the form, consenting to the election — name, SSN, ownership percentage, and shares (or membership interest) owned. Multi-member LLCs with custom profit splits need a careful look here, because non-pro-rata distributions can violate the one-class-of-stock rule.

- Part II — Fiscal year selection (only if not using a calendar year — most S-Corps use a calendar year; a fiscal year requires IRS approval).

- Part III — Qualified Subchapter S Trust (QSST): Only complete if a trust is a shareholder.

- File by mail or fax to the IRS service center for your state. The IRS sends an acceptance letter (CP261) within roughly 60 days — keep it forever.

After Approval: The Payroll and Compliance Rhythm

Once the election is accepted, you are an employee of your own company — and an accepted election with no W-2 wages is the worst of both worlds. The ongoing rhythm looks like this:

- Run official payroll on a regular schedule (monthly or bi-weekly), with federal and state withholding and FICA deposits — we set clients up on automated payroll (ADP is our preferred partner) so this runs on rails.

- File Form 941 quarterly and Form 940 annually, and issue yourself a W-2 each January.

- File Form 1120-S by March 15, which issues you a Schedule K-1 for your personal return.

- Keep the books clean: a separate business bank account, payroll properly categorized, and distributions tracked against your basis.

Most owners find the structure forces better financial hygiene — real payroll, real books, a real quarterly rhythm. That discipline is also what makes the next strategies possible: the salary you formalize becomes the contribution base for a Solo 401(k), an Accountable Plan, and family employment strategies.

Common Mistakes That Trigger Audits

We've seen hundreds of S-Corp returns done wrong. These are the mistakes that cost business owners the most.

Mistake #1: Taking Zero Salary (All Distributions)

This is the single fastest way to get audited. If you're performing services for the S-Corp and taking distributions but paying yourself $0 in salary, the IRS will reclassify those distributions as wages — and assess back payroll taxes, penalties, and interest. Tax Court has ruled against this repeatedly (see Watson v. Commissioner, Radtke v. United States). Solution: Always run payroll and pay yourself a reasonable salary. No exceptions.

Mistake #2: Setting Salary Unreasonably Low

A software consultant earning $300,000 through their S-Corp who pays themselves $30,000 is asking for trouble. The IRS doesn't publish a minimum salary, but they compare your compensation to market rates for the services you provide. If the salary is far below what an employee would earn, the IRS will reclassify distributions. Solution: Conduct a formal reasonable compensation study using BLS data and industry benchmarks.

Mistake #3: Not Running Actual Payroll

Some owners "pay themselves" by writing a check from the business account and calling it salary — without processing it through a payroll system. This means no federal/state withholding, no quarterly 941 filings, no W-2 at year-end, and no employer FICA deposits. The IRS treats this as if you never paid yourself at all. Solution: Use a payroll provider (ADP, Paychex) from day one. This is non-negotiable for S-Corp compliance.

Mistake #4: Missing the Election Deadline

You file your Form 2553 on April 1 thinking it applies to the current year. It doesn't. The deadline is March 15 for calendar-year entities. You just lost a full year of S-Corp savings — potentially $15,000–$25,000. Solution: File Form 2553 immediately upon formation (within 75 days) or before March 15 of the tax year. If you've missed the deadline, contact us about late election relief under Rev. Proc. 2013-30.

Mistake #5: No Reasonable Compensation Documentation

Even if your salary is perfectly reasonable, if you can't prove it's reasonable, you're at a disadvantage in an audit. The IRS bears the burden of proving the salary is unreasonable — but only if you have documentation. Without a formal study on file, you're relying on after-the-fact arguments. Solution: Prepare a written compensation analysis annually. Keep it in your tax file. This is your audit insurance.

Mistake #6: Commingling Personal and Business Funds

Using the S-Corp bank account for personal expenses (or vice versa) can jeopardize your limited liability protection and creates accounting nightmares. More importantly, the IRS may argue that you're treating the entity as an alter ego — which undermines the entire S-Corp structure. Solution: Maintain a dedicated business bank account. All salary is paid through payroll. All distributions are recorded as formal distributions. Personal expenses are never run through the business account.

The Trust Fund Recovery Penalty: Personal Liability

If the IRS reclassifies your S-Corp distributions as wages, the unpaid payroll taxes (specifically the employee's share of FICA and income tax withholding) become a "trust fund" liability. Under IRC §6672, the Trust Fund Recovery Penalty (TFRP) can be assessed personally against you as the "responsible person" — meaning it pierces the corporate veil. This penalty equals 100% of the unpaid trust fund taxes and cannot be discharged in bankruptcy. This is not theoretical — we've seen it happen to S-Corp owners who took distributions without running payroll.

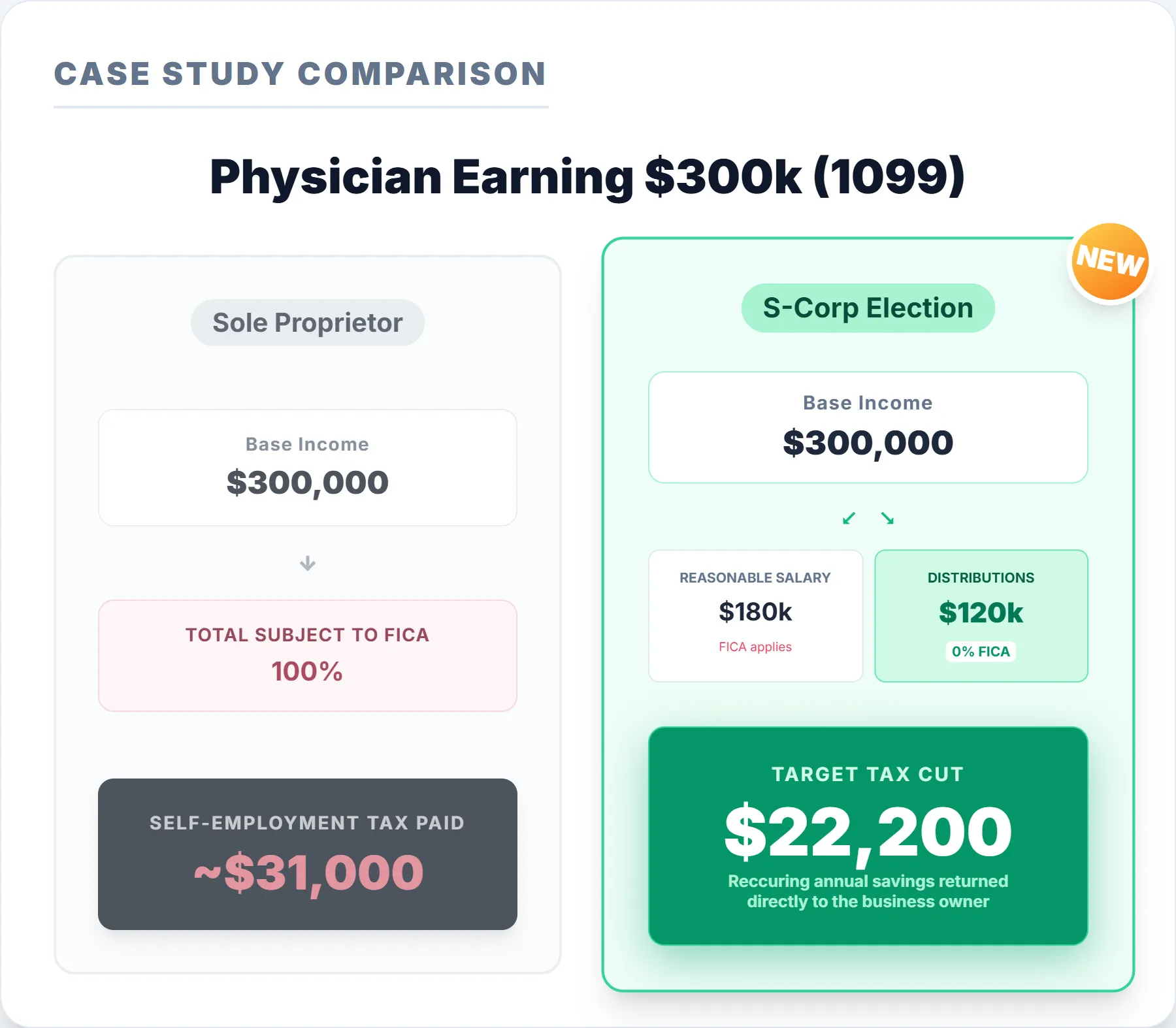

Case Study: The Locum Tenens Physician

How a 1099 physician saved $22,000+ per year in self-employment tax with a single Form 2553.

S-Corp Case Study: $22K Saved Per Year (Physician 1099 Income)

Dr. Patel is an anesthesiologist working locum tenens assignments across three states. All income is 1099 — no employer withholds taxes. Before coming to Taxstra, Dr. Patel was filing as a sole proprietor (Schedule C) and paying approximately $31,000 per year in self-employment tax alone — on top of federal and state income taxes.

The Structure

Formed a single-member LLC in Wyoming. Filed Form 2553 to elect S-Corp taxation. Opened a dedicated business bank account.

The Salary

Based on BLS data and Medscape anesthesiologist compensation surveys, we set the reasonable salary at $180,000 — the 50th percentile for employed anesthesiologists nationally, adjusted for the locum tenens context.

The Savings

The remaining $120,000 in profit flowed through as distributions — saving $22,200+ in SE tax annually. We also set up a Solo 401(k) to shelter an additional $69,000 in pre-tax income.

Tax Savings Summary (Annual, Recurring)

Annual SE Tax Savings

$22,200

Recurring every year. After compliance costs (~$3,500/yr), net savings of ~$18,700/yr.

S-Corp vs. LLC vs. C-Corp: When to Use Each

The S-Corp election isn't always the right choice. Understanding when to use each entity structure is critical for optimizing your overall tax position. For side-by-side breakdowns, see our sole proprietorship vs. S-Corp comparison, our full S-corp vs C-corp breakdown, and the LLC vs. S-Corp guide.

| Factor | Sole Prop / Disregarded LLC | S-Corp (LLC + 2553) | C-Corp |

|---|---|---|---|

| SE Tax on Profit | 15.3% on 100% | Only on salary portion | No SE tax (but double taxation on dividends) |

| Compliance Cost | Lowest | Medium ($2K–$5K/yr) | Highest |

| QBI Deduction (§199A) | Full profit qualifies | Only distributions qualify | Not available (C-Corp income) |

| Payroll Required? | No | Yes — mandatory | Yes — if paying shareholders |

| Filing Deadline | April 15 (Sch C) | March 15 (Form 1120-S) | April 15 (Form 1120) |

| Best For | < $50K net profit | $50K–$500K net profit | Retained earnings, VC-backed, or high-growth exit plans |

| Ownership Flexibility | Unlimited | ≤ 100 shareholders, US only, one class of stock | Unlimited — any structure |

For the vast majority of self-employed professionals, 1099 contractors, and small business owners earning $50K–$500K in net profit, the LLC + S-Corp election is the optimal structure. It gives you the liability protection of an LLC, the payroll tax savings of an S-Corp, and the simplicity of pass-through taxation. The C-Corp only makes sense in specific situations — typically involving retained earnings for growth, venture capital, or a planned exit at the 21% corporate rate.

Section 199A QBI Deduction: The S-Corp Planning Variable

The One Big Beautiful Bill Act permanently extended the Section 199A Qualified Business Income (QBI) deduction, which allows a deduction of up to 20% of qualified business income. This is permanently relevant to S-Corp planning because of the salary-distribution tension:

The S-Corp QBI Tradeoff

Your W-2 salary does not qualify for the QBI deduction — only the K-1 pass-through income does. A higher salary saves more SE tax but reduces QBI. A lower salary maximizes QBI but risks IRS reclassification. The optimal salary balances both — and the answer is different for every client based on income level, filing status, and whether you're above the QBI phase-out thresholds ($201,750 single / $403,500 MFJ for 2026).

For most S-Corp owners below the QBI phase-out thresholds, the SE tax savings from a properly set salary exceed the lost QBI deduction. But for high-income owners near or above the thresholds, the QBI deduction may phase out regardless — making the SE tax savings the dominant variable. This is why we model both scenarios for every client.

Accountable Plans: An Additional S-Corp Benefit

Is the S-Corp Election Right for You?

The S-Corp is one of the most powerful elections available — but it's not for everyone. Here's how to tell.

Perfect Candidates

Not a Fit If...

Why High-Income Professionals Choose Taxstra for S-Corp Strategy

We don't just file Form 2553. We build the entire S-Corp infrastructure — and keep it compliant year after year.

The S-Corp election itself takes five minutes to file. The implementation — payroll setup, reasonable compensation analysis, QBI optimization, entity structuring, ongoing compliance — is where most CPAs drop the ball. We handle all of it.

- We prepare the Form 2553 election — including late elections under Rev. Proc. 2013-30 when clients come to us after the deadline

- We conduct a formal reasonable compensation study — documented with BLS data, industry benchmarks, and Tax Court factor analysis — and update it annually

- We set up and monitor payroll — ensuring quarterly 941s are filed, W-2s are issued, and FICA deposits are made on time

- We optimize the salary-QBI tradeoff — modeling both variables to find the salary that maximizes total after-tax income, not just SE tax savings

- We layer complementary strategies — Solo 401(k), Accountable Plans, STR Loophole, and retirement plan stacking on top of the S-Corp foundation

- Year-round engagement — quarterly check-ins, mid-year salary adjustments if income changes, and proactive outreach when tax law creates new opportunities

Featured on The White Coat Investor

Related Strategies

The S-Corp election is often the foundation of a broader tax strategy. Here are complementary strategies our clients frequently pair with it:

- Solo 401(k) — Shelter up to $69,000+ pre-tax through employer + employee contributions (S-Corp required for employer match)

- Accountable Plans — Tax-free reimbursements for home office, cell phone, internet, travel, and education

- STR Loophole — Offset W-2 and S-Corp income with accelerated real estate depreciation

- Entity Structure Optimization — Multi-entity planning for those with both active businesses and real estate

- Real Estate Professional Status (REPS) — Unlock unlimited passive losses against S-Corp and W-2 income

- 100% Bonus Depreciation — Accelerate asset purchases through the S-Corp for immediate deductions

Frequently Asked Questions

Not Sure If the S-Corp Election Makes Sense for You?

Tell us your annual net profit and current entity structure — we'll send back a projected savings analysis within 24 hours. No call required.

Every Quarter You Wait Is a Quarter of SE Tax You Didn't Have to Pay.

The S-Corp election is a straightforward, high-impact strategy for any self-employed professional netting $50K+ per year. We handle the election, payroll setup, reasonable compensation analysis, and ongoing compliance — so you save money without adding complexity to your life.

Book a Free ConsultationNo obligation • Takes 30 minutes • Done over the phone

About the Author

Bryan Martin, CPA • Licensed Real Estate Broker

Bryan is the founder of Taxstra PLLC, a CPA firm specializing in tax strategy for high-income earners, real estate investors, and business owners. He holds both a CPA license and a real estate broker license, giving him a unique dual perspective on business and real estate tax strategy. Bryan was featured on The White Coat Investor Podcast (Episode #459) and works with clients nationwide from his base in Springfield, IL.

Learn more about Bryan →