The Hard Truth About REPS

Real Estate Professional Status is among the most frequently litigated tax positions in the entire Internal Revenue Code. The IRS knows that when a physician or attorney earning $500,000 in W-2 income suddenly reports $100,000 in rental losses, something is probably wrong. They audit accordingly.

Most people who claim REPS shouldn't. Many who legitimately qualify still lose in audit because their documentation falls apart under scrutiny. The Tax Court is littered with cases where taxpayers spent the money, took the deduction, and then watched it all unravel because they couldn't prove their hours.

Your REPS Advisor: Bryan Martin

CPA & Licensed Real Estate Broker

Bryan holds a rare dual qualification as both a practicing CPA and a licensed Managing Broker. He doesn't just know the tax code—he understands the operational reality of real estate. He has helped dozens of investors qualify for REPS and defend their elections under IRS scrutiny.

We turn away more REPS claims than we file. Not because we're conservative, but because the math doesn't work for most people—and we won't help clients take positions that collapse under examination. If you work a full-time job, you almost certainly cannot qualify yourself. That's not pessimism; that's arithmetic.

This guide exists because REPS is genuinely powerful when done right. A properly structured REPS election can save $50,000 or more annually for the right household. But done wrong—or documented poorly—it invites penalties, interest, and the stress of an audit you're likely to lose.

Read this guide to understand whether REPS is realistic for your situation, what it actually requires, and how to execute it in a way that holds up.

This guide is for you if:

- You or your spouse can realistically spend 750+ hours on real estate

- Your household has one spouse who works part-time or not at all

- You own rental properties with significant depreciation or losses

- You want to offset W-2 income, not just defer taxes

This guide is NOT for you if:

- Both spouses work full-time in non-real-estate careers

- You have one or two rental properties managed by a PM

- You're looking for a "loophole" that requires no real time commitment

TL;DR: How REPS Actually Works

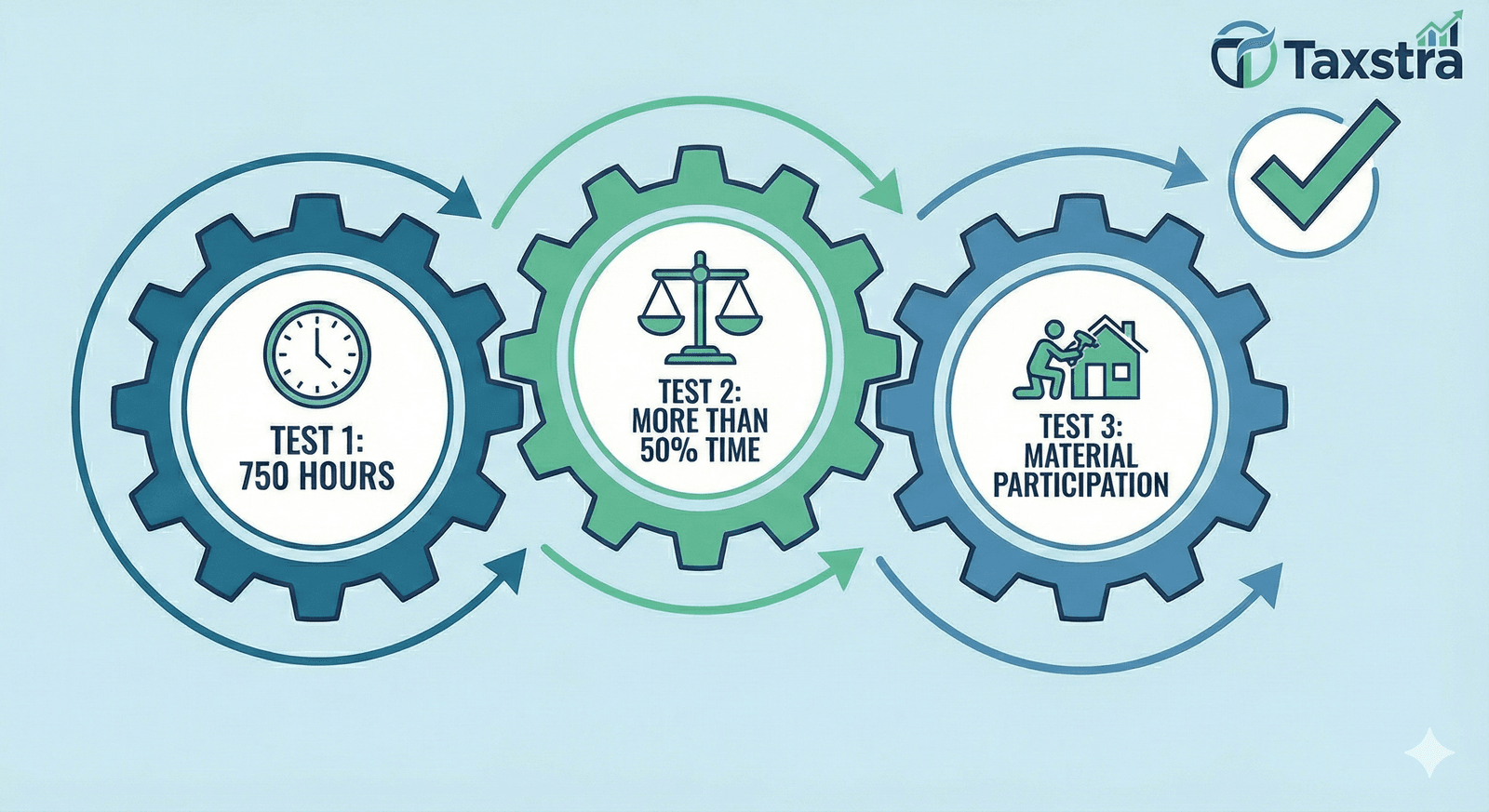

To qualify as a Real Estate Professional, one spouse must pass three tests: spend more than 750 hours in real estate activities, spend more than 50% of their total working time in real estate, and materially participate in each rental activity.

The spouse rule: For married couples filing jointly, only one spouse needs to qualify. If one spouse works part-time or stays home to manage real estate, they can qualify—and the losses offset the high-earning spouse's W-2 income.

Critical requirements: You must file a grouping election to treat all properties as one activity, and you must keep contemporaneous time logs. Without both, even legitimate REPS claims fail in audit.

What Real Estate Professional Status Actually Is

Real Estate Professional Status is an IRS tax classification—not a license, certification, or professional designation. You don't need real estate training or credentials. It's purely about how you spend your time.

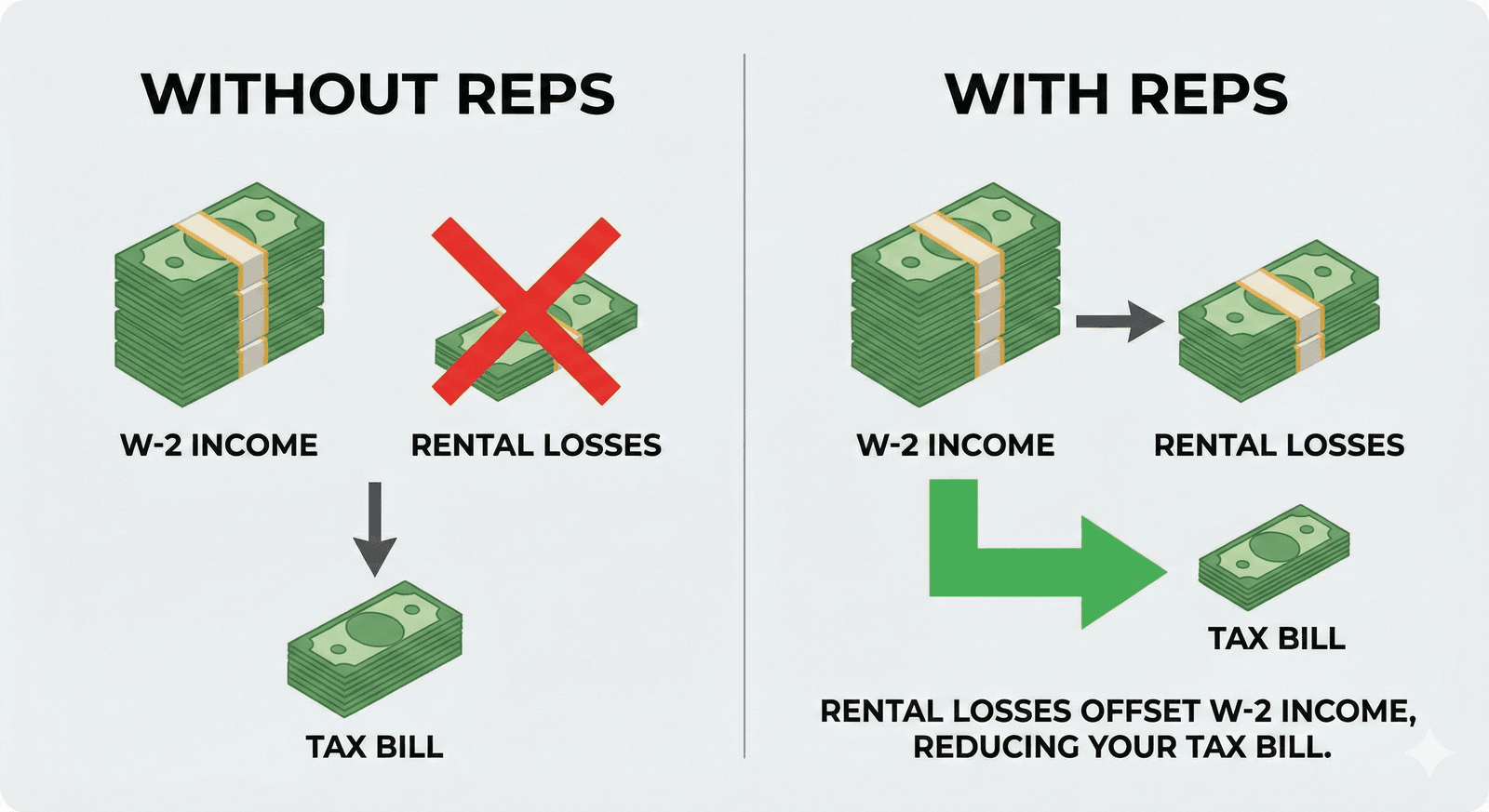

By default, the IRS considers all rental real estate activity to be "passive"—even if you spend significant time managing your properties. Under passive activity rules, you can only deduct rental losses against other passive income. No passive income? Those losses get "suspended" and carried forward, potentially for years, until you sell the property.

REPS changes that treatment. If you qualify as a real estate professional and materially participate in your rental activities, those activities are no longer automatically passive. Your rental losses become "non-passive"—deductible against any income, including W-2 wages, business income, and even capital gains.

Why REPS Matters Financially

The financial impact of REPS can be substantial. Consider the math:

REPS Savings Calculator

Estimate how much you could save by reclassifying passive losses.

Estimated Annual Tax Savings

Based on estimated federal marginal rate + 3.8% NIIT + 4.95% IL state tax. Actual savings may vary.

Want to see if you qualify? Book a call- Offset W-2 income with rental losses. Without REPS, $50,000 in rental losses provides zero tax benefit if you lack passive income. With REPS, that $50,000 directly reduces your taxable income. At the top federal bracket plus state taxes, that's $20,000 or more in annual savings.

- Unlock suspended passive losses. If you've accumulated passive losses from prior years that you couldn't use, qualifying for REPS can release those losses against current income.

- Avoid the 3.8% Net Investment Income Tax. High earners pay an additional 3.8% tax on net investment income, including passive rental income. REPS combined with material participation can eliminate this. On $100,000 of rental income, that's $3,800 saved annually.

- Supercharge cost segregation. A cost segregation study on a $1 million property might generate $200,000 to $300,000 in accelerated first-year depreciation. Without REPS, those losses are passive and suspended. With REPS, they offset W-2 income immediately.

Now that you understand what REPS changes, here's why it fails for most people—and why the IRS scrutinizes these claims so heavily.

Why REPS Fails for Most W-2 Earners

Before we go further, understand this: the math is unforgiving.

To qualify, you must spend more than 50% of your total working time in real estate. If you work a full-time job, that means spending more hours on real estate than you do at work. Here's what that looks like:

| Your W-2 / Non-RE Hours | Real Estate Hours Required |

|---|---|

| 1,000 (part-time) | 1,001+ |

| 1,500 | 1,501+ |

| 2,000 (full-time) | 2,001+ (Nearly Impossible) |

| 2,500 | 2,501+ (Impossible) |

If you work a standard full-time job—roughly 2,000 hours per year—you need to spend more time on real estate than on your job. That's essentially two full-time commitments. Very few people can genuinely do this.

This is why physicians, attorneys, executives, and most high-income professionals cannot qualify themselves. But their spouses often can—and that's where the strategy becomes viable.

If you personally can't clear the time tests, stop here. If your spouse can, keep reading.

The Three Tests You Must Pass

Qualifying as a real estate professional requires satisfying three separate tests. Miss any one of them, and you don't qualify.

Test 1: The 750-Hour Test

You must perform more than 750 hours of services during the tax year in "real property trades or businesses" in which you materially participate. This includes property development, construction, acquisition, rental operations, management, leasing, and brokerage.

Test 2: The More-Than-50% Test

More than half of the personal services you perform in all trades or businesses during the tax year must be in real property trades or businesses where you materially participate. This is the test that eliminates full-time W-2 employees. If you work 2,000 hours at your day job, you need more than 2,000 hours in real estate to pass.

Test 3: Material Participation in Each Rental Activity

Even after passing the first two tests, you must also materially participate in each rental real estate activity where you want non-passive treatment. The IRS provides seven tests for material participation. You only need to meet one:

- 500-hour test: You participated more than 500 hours during the year.

- Substantially all test: Your participation was substantially all of the participation by all individuals.

- 100-hour / no-one-more test: You participated more than 100 hours, and no one else participated more than you.

- Significant participation test: The activity is a "significant participation activity" and your total hours in all such activities exceed 500.

- Five-of-ten-years test: You materially participated in any 5 of the prior 10 tax years.

- Personal service activity test: For personal service activities, material participation in any 3 prior years.

- Facts and circumstances test: Based on all facts and circumstances, you participated on a regular, continuous, and substantial basis.

For most landlords, the cleanest path is the 500-hour test—documented carefully. But this creates a challenge: if you own 10 properties and spend 500 total hours, you average only 50 hours per property. You'd fail the 500-hour test on every single one.

That's where the grouping election becomes essential.

The Spouse Strategy for High-Income Households

Here's the insight that makes REPS accessible to physician, attorney, and executive households: for married couples filing jointly, only one spouse needs to qualify as a real estate professional.

If one spouse qualifies for REPS, the rental losses on the joint return can be treated as non-passive—even if the other spouse works 60 hours a week as a surgeon. The qualifying spouse doesn't need to earn anything from real estate. They just need to spend the time.

This creates a realistic path for dual-income households where one spouse has stepped back from their career, works part-time, or manages the household. A spouse who works 800 hours at a part-time job and spends 1,000 hours on real estate qualifies easily: 1,000 exceeds both 750 and 800.

The strategy works best when the qualifying spouse genuinely takes on the role of managing the real estate portfolio—screening tenants, coordinating maintenance, overseeing renovations, handling the books. This isn't a paper exercise. The IRS will want to see that the qualifying spouse was actually doing the work.

Example: The Smith Household

- • Dr. Smith earns $400,000 as a physician, working 2,200 hours/year

- • Mr. Smith works part-time (800 hours/year) at a consulting job

- • Mr. Smith spends 1,000 hours managing their rental portfolio

Mr. Smith qualifies:

- 750-hour test: 1,000 > 750

- More-than-50% test: 1,000 RE hours > 800 non-RE hours

- Material participation: he manages the properties directly

Because they file jointly, the household uses rental losses to offset Dr. Smith's $400,000 W-2 income.

Important precision on combining hours: Spouses can combine their hours for the material participation tests (e.g., both contribute to getting over 500 hours for a property). However, the 750-hour and more-than-50% tests must be satisfied by one spouse individually. You cannot add both spouses' hours to get to 750.

Even with perfect spouse qualification, two failure points destroy more REPS claims than anything else: the grouping election and documentation. Both require attention before you ever file.

The Grouping Election

Critical: This Is the Most Commonly Missed Step

Without the grouping election, each rental property is treated as a separate activity. You must prove material participation for each property individually. If you own 10 properties and spend 500 total hours, you average 50 hours each—failing the 500-hour test on every single one. The grouping election lets you treat all properties as a single activity.

Under IRC Section 469(c)(7)(A), a qualifying real estate professional can elect to treat all rental real estate interests as a single activity. With this election, your 500 total hours across 10 properties count as 500 hours in one combined activity—passing the 500-hour material participation test.

The election must be filed with your original, timely-filed return (including extensions) for the year you want it to apply. You cannot amend it in later. Miss the deadline, and you may have to wait until the next tax year.

Sample election language:

"I hereby make an election pursuant to IRC Section 469(c)(7)(A). I am a qualifying taxpayer for the tax year and elect to treat all of my interests in rental real estate as a single activity, effective for tax year 2025 and all subsequent years."

Once made, the grouping election binds you for all future years unless your facts and circumstances materially change. This is rarely a problem for taxpayers who intend to stay active in real estate, but understand that it's not easily reversible.

Documentation: The Audit Shield (or Your Undoing)

Without Proper Documentation, You Will Lose

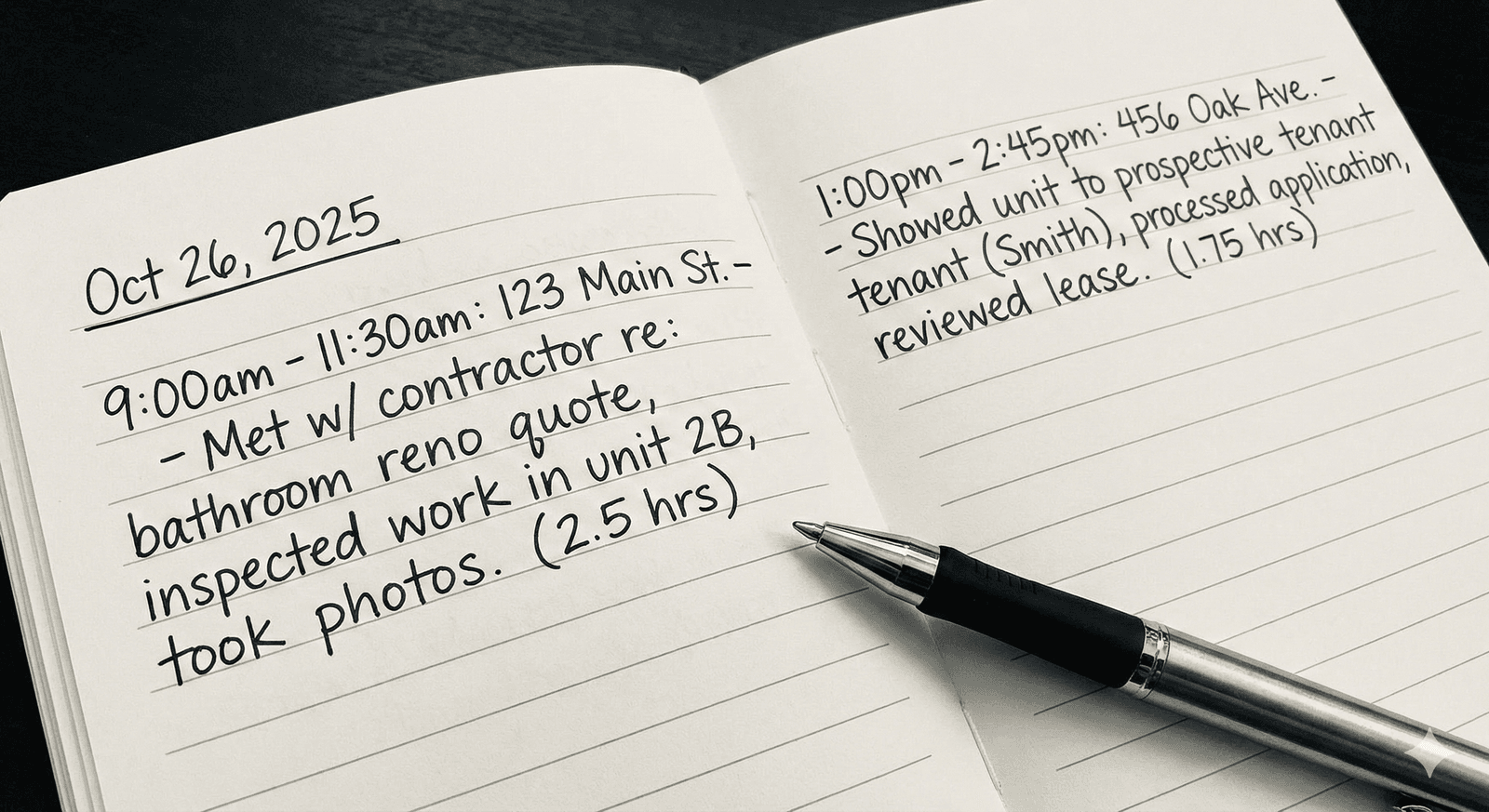

The IRS audits REPS claims aggressively, especially for high-income taxpayers reporting significant W-2 income alongside real estate losses. The Tax Court has repeatedly held that after-the-fact reconstructions are not sufficient. You need contemporaneous records—created at or near the time the work was performed.

Your time log is your defense. When the IRS questions your 800 hours, you need to show them a detailed record—not a spreadsheet you created the week before the audit.

A defensible time log includes the date of each activity, the property or activity involved, specific tasks performed, and time spent (start and end times are ideal). Generic entries like "property management - 3 hours" won't hold up. "123 Main St - met contractor to review bathroom renovation quote, inspected work in unit 2B, photographed damage - 10am to 12:30pm" will.

Beyond the log itself, supporting evidence strengthens your position: calendar entries, emails with contractors and tenants, text messages, receipts, mileage logs, photos, invoices, bank statements. The more you can corroborate your log with third-party records, the harder it is for the IRS to challenge your hours.

Red flags the IRS looks for:

- Generic descriptions: Vague entries suggest fabrication.

- Suspiciously round numbers: Exactly 800 hours, or exactly 4 hours every Saturday, looks manufactured.

- Unrealistic totals: 1,500 hours on a single-family rental strains credibility.

- Internal inconsistency: Your log shows you working weekends while your credit card shows you on vacation.

Even with perfect structure, documentation is what wins or loses in audit. Log your hours weekly—not annually. Use an app if that helps. Save everything.

What Counts as Qualifying Hours

Not all time spent "on" real estate counts toward REPS. The IRS draws a clear line between activities that qualify and those that don't.

Hours That Count

- Advertising vacancies and showing units

- Screening tenants and processing applications

- Negotiating and executing leases

- Collecting rent and handling late payments

- Coordinating repairs and maintenance

- Conducting property inspections

- Overseeing renovations, meeting contractors

- Driving to/from properties for business purposes

Hours That Don't Count

- Researching potential investments

- Analyzing deals you don't acquire

- Reading real estate books or listening to podcasts

- Attending seminars for general education

- Hours worked by property managers you hire

- Time spent by contractors (unless you actively supervise)

- W-2 employment in real estate (unless you own 5%+ of the employer)

A note on property manager oversight: If you hire a property manager, their hours don't count toward yours. However, if you remain genuinely involved—reviewing and approving tenant applications, making capital decisions, conducting periodic inspections, overseeing the manager's work—your supervisory hours may count. The IRS scrutinizes this, so document your involvement carefully.

3 REPS Mistakes That Trigger IRS Audits

The "Impossible" Schedule

Claiming REPS while working a full-time W-2 job (2,000+ hours). The IRS algorithms flag this immediately because it's mathematically improbable to work 2,000 job hours AND 2,001 real estate hours.

The "Back-of-Napkin" Log

Failing to keep a contemporaneous time log. Creating a calendar during the audit is fatal. The Tax Court routinely rejects "ballpark estimates" and reconstructed logs.

Counting "Research"

Padding hours with Zillow research, education, or investor seminars. These are "investor hours," NOT "real property trade or business hours," and they will be disallowed.

We help you avoid all three with proper planning and documentation.

REPS vs. The "Short-Term Rental Loophole"

If you can't hit the 750-hour test or work a full-time job, you might still qualify for non-passive losses through Short-Term Rentals (STRs). The rules are completely different.

| Factor | REPS (Long-Term) | STR Loophole |

|---|---|---|

| Property Type | Residential / Commercial | Avg stay ≤ 7 days (Airbnb) |

| Time Requirement | 750+ Hours | 100+ Hours (Material Participation) |

| W-2 Job Compatibility | Very Difficult (unless spouse) | Compatible |

| Best For | Spouse manages portfolio | High-income earners (single or dual) |

Who actually qualifies?

REPS is not a loophole for everyone. It is a specific status for valid real estate businesses. You likely qualify if you can check these four boxes:

Spouse Availability

One spouse works part-time in RE or manages the portfolio while the other earns W-2 income.

Portfolio Scale

You own enough properties (usually 3-5+) to justify spending 750 hours a year managing them.

Time Commitment

One of you can dedicate ~15 hours every single week to operations and management.

Tax Appetite

You have significant W-2 or business income to offset (usually $300k+ household income).

Do You Qualify?

Do you or your spouse work a full-time W-2 job (non-real estate)?

Your Roadmap to Tax Savings

Assess Eligibility

Review your hours, job status, and projected rental losses to ensure REPS is viable.

"We analyze your W-2 hours vs. potential real estate hours. If the math doesn't work, we stop here—saving you time and audit risk."

"The IRS rejects retroactive logs. We help you set up a compliant tracking system that takes less than 5 minutes a week."

Setup Time Tracking

Implement a contemporaneous logging system (Toggl, spreadsheet, or physical journal) immediately.

Make Grouping Election

File the Section 469(c)(7)(A) election with your tax return to combine all rental activities.

"This one-time election is critical. Without it, you must pass the 500-hour test for *each* property individually."

"Most tax software misses this election by default. We double-check every return to ensure Section 469(c)(7)(A) is properly attached."

File Return (With Election)

Claim your losses on Schedule E. Ensure the grouping election is attached to your return.

Maintain Records

Keep your time logs, emails, and evidence of participation for at least 3 years to defend against audit.

"In an audit, the burden of proof is 100% on you. We recommend digital backups of all logs and receipts."

Before You Schedule

REPS isn't for everyone. Before booking a call, honestly assess your situation:

- •If neither spouse can realistically hit 750+ hours, REPS won't work for you.

- •If your spouse can qualify, schedule a call to map out the structure.

- •If you have short-term rentals, the STR loophole may be a better fit.