The STR Loophole:

Offset W-2 Income with Rental Losses

The most effective way for high-income W-2 earners to legally wipe out $100K–$300K+ in taxable income using real estate — now with 100% bonus depreciation permanently restored under the OBBBA.

TL;DR — The STR Loophole in 60 Seconds

The STR Loophole (Treas. Reg. §1.469-1T(e)(3)(ii)(A)) lets short-term rental owners reclassify rental losses as non-passive — offsetting W-2 wages dollar-for-dollar. You need three things: an average guest stay of 7 days or fewer, proof of material participation (100+ hours/year), and a cost segregation study to accelerate depreciation. With 100% bonus depreciation permanently restored under the OBBBA, a typical $1M STR property generates $200K–$300K in Year 1 deductions against active income — no Real Estate Professional Status required.

What is the STR Loophole?

The Short-Term Rental (STR) Loophole — sometimes called the Airbnb tax loophole or VRBO tax deduction strategy ��— is a legal tax strategy rooted in Treas. Reg. §1.469-1T(e)(3)(ii)(A) that allows real estate investors to reclassify rental losses as non-passive — meaning those losses can directly offset W-2 wages, business income, and other active income on your tax return.

For most rental property owners, losses are trapped by the passive activity loss rules under IRC §469. You can't use them against your paycheck. The STR Loophole changes that — without requiring Real Estate Professional Status (REPS), which demands 750+ hours per year and is nearly impossible for anyone with a full-time job.

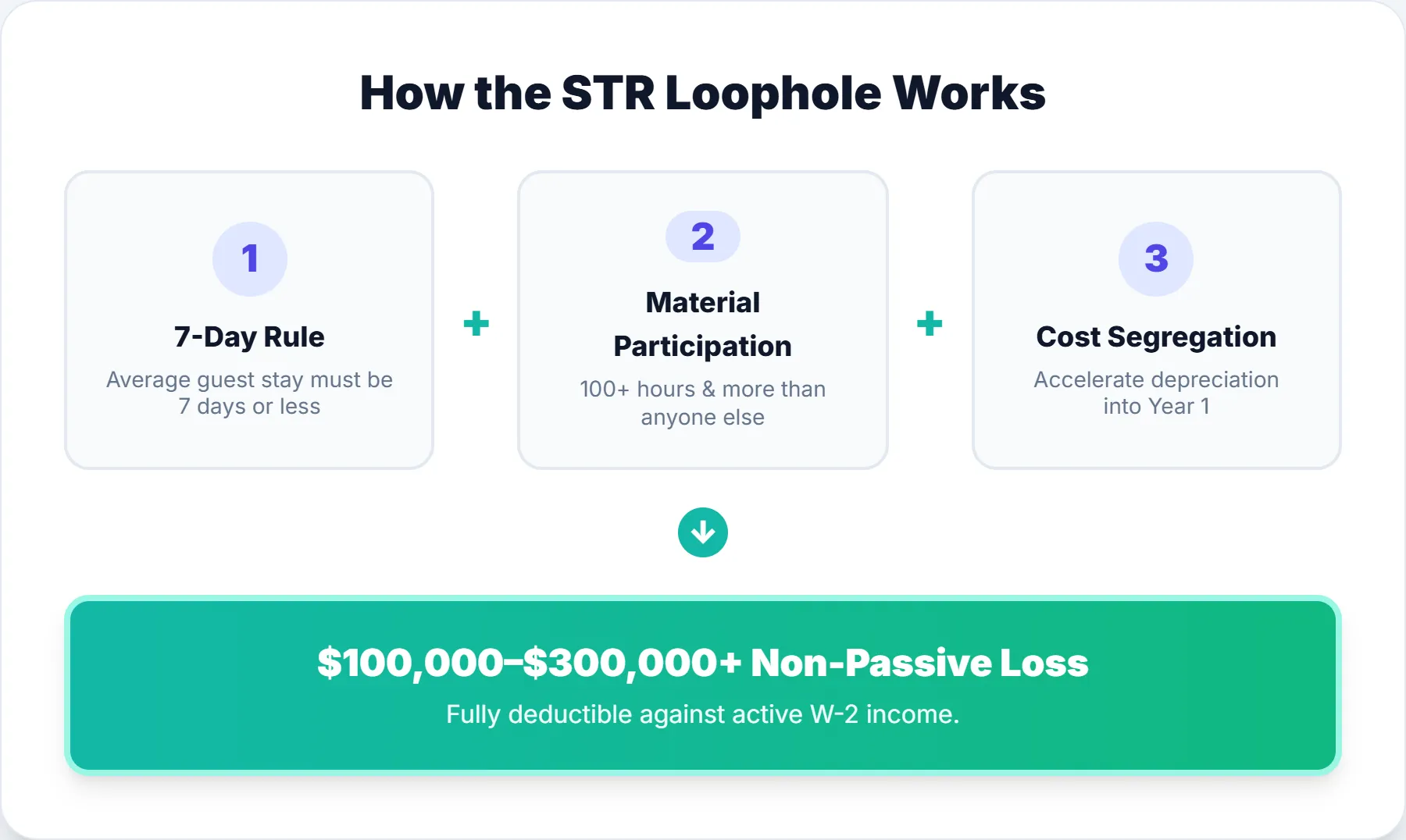

Instead, the STR Loophole requires three things: an average guest stay of 7 days or less, proof that you materially participated in managing the property, and a cost segregation study to accelerate depreciation into Year 1. With 100% bonus depreciation now permanently restored under the One Big Beautiful Bill Act (OBBBA), these create paper losses of $100,000–$300,000+ that flow through to your personal return and reduce your tax bill dollar-for-dollar.

$100K–$300K+

Typical Year 1 tax deduction with 100% bonus depreciation (OBBBA)

No REPS

No need for 750+ hours — just 100+ hours of material participation

W-2 Friendly

Designed for physicians, tech workers, and high-income employees

This guide covers everything you need to know: the legal foundation for the loophole, all seven Material Participation tests, the alternative non-rental classification rules beyond the 7-day average, a detailed case study with $131,400 in Year 1 tax savings under 100% bonus depreciation, and the common mistakes that cause the strategy to fail under audit. Whether you're considering your first STR purchase or you already own a property you want to optimize, this is the most complete guide available — fully updated for the One Big Beautiful Bill Act (OBBBA).

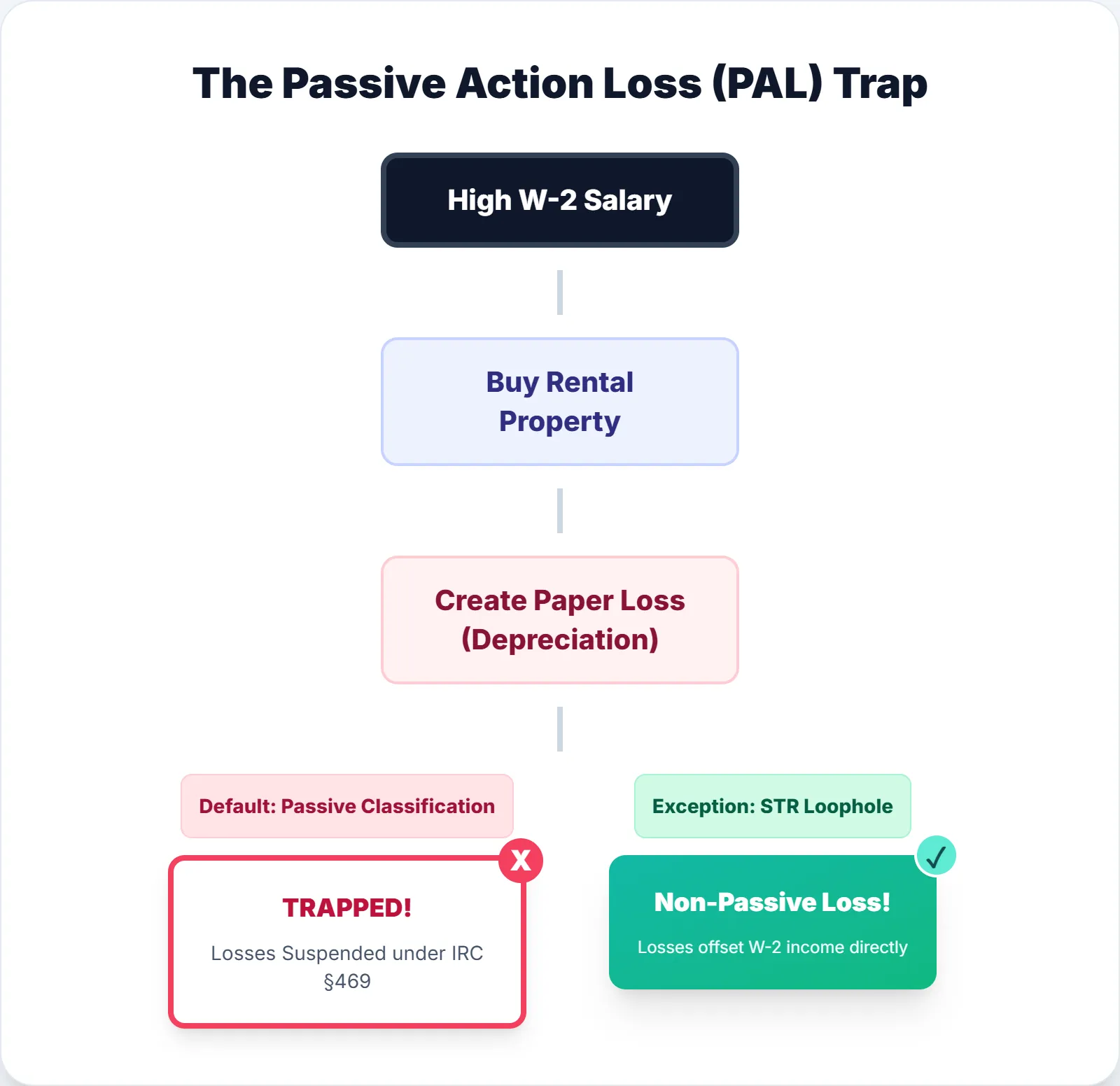

The Passive Loss Trap

Why most high-income earners fail at real estate tax strategy — and what the IRS doesn't want you to figure out.

You make a lot of money. You pay a lot of taxes. Naturally, you look to real estate to lower that bill. You buy a rental property — maybe a condo or a single-family home — expecting a big write-off.

Then your CPA gives you the bad news: "You can't use those losses."

This is the Passive Activity Loss (PAL) trap. Under IRC Section 469, all rental activity is classified as "passive" by default. Passive losses can only offset passive income (like other rental income). They cannot touch your active W-2 salary or business income.

"So I have a $50,000 paper loss from depreciation, but I still pay tax on my $500,000 salary?" — Yes. Unless you use the Loophole.

There are traditionally two ways around this trap:

| Long-Term Rental | Short-Term Rental (The Loophole) | |

|---|---|---|

| Lease Terms | 30+ days | Average stay 7 days or less |

| IRS Classification | Passive (rental activity) | Non-passive (business activity) |

| Losses Offset W-2? | No — trapped as passive | Yes — immediately usable |

| REPS Required? | Yes (750+ hours/year) | No — just Material Participation |

| Best For | Full-time RE investors | W-2 earners with day jobs |

| Key Regulation | IRC §469 | Treas. Reg. §1.469-1T(e)(3)(ii)(A) |

The Real Estate Professional Status (REPS) path requires 750+ hours per year in real estate — essentially impossible if you have a full-time W-2 job. The STR Loophole is the alternative that makes this accessible to physicians, tech professionals, and other high earners.

If you're already familiar with passive vs. active loss rules, you know how frustrating it is to have paper losses you can't use. The STR Loophole is the most practical way around this for W-2 taxpayers.

How the STR Loophole Works

Three tests. Pass all three, and your rental losses become non-passive — offsetting W-2 income directly.

Why This Works: The Three-Bucket Rule

To understand why the loophole exists, picture how the IRS sorts income. Every dollar you earn lands in one of three buckets: active (W-2 wages, 1099 income, business profits), portfolio (interest, dividends, capital gains), and passive (rental income and most limited-partner income). Losses generally cannot cross the bucket walls — a passive loss can only offset passive income. That's why a physician earning $500,000 with a $50,000 rental loss still pays tax on the full $500,000: the loss is trapped in the passive bucket, doing nothing.

The STR Loophole exploits a precise exception to that sorting system: activities where the average customer use is 7 days or fewer are not defined as rental activities under the passive loss rules at all. They're treated as a business. And if you materially participate in that business, its losses land in the active bucket — crossing the wall and offsetting your W-2, 1099, or business income directly.

STR Loophole Requirements: The Three Tests

To convert your short-term rental losses from passive to non-passive, you must satisfy three independent requirements. Miss any one of them and the losses stay trapped.

STR Loophole at a Glance

Test 1: The 7-Day Rule (Primary Path)

Under Treas. Reg. §1.469-1T(e)(3)(ii)(A), if the average period of customer use is 7 days or less, the property is not treated as a "rental activity" for passive loss purposes. It's treated as a business — and business losses are not subject to the passive activity rules.

The average is calculated by dividing total rental days by total number of bookings. Example: 100 days rented across 20 stays = average of 5 days. You pass.

Calculating the Average Correctly

Only rented days count — not days the property sits vacant. If you have 15 bookings totaling 90 nights, the average is 90 ÷ 15 = 6 days (you pass). Personal-use days are excluded from the calculation entirely.

Be especially careful with monthly bookings. One 30-day stay among ten 3-day stays would yield: (30 + 30) ÷ 11 = 5.45 days — you'd still pass. But two 30-day stays could push you over 7.

Beyond the 7-Day Rule: Alternative Non-Rental Classifications

The 7-day rule is the most common path, but it's not the only way to escape the rental activity classification under IRC §469. Treas. Reg. §1.469-1T(e)(3)(ii) provides four total exceptions. If you meet any one of them, the property is not a rental activity:

| Exception | Regulation | What It Requires | Best For |

|---|---|---|---|

| (A) 7-Day Rule | §1.469-1T(e)(3)(ii)(A) | Average guest stay ≤ 7 days | STR/Airbnb hosts (most common) |

| (B) Significant Services | §1.469-1T(e)(3)(ii)(B) | Average stay ≤ 30 days AND significant personal services provided | Boutique hotels, B&Bs, furnished MTRs with concierge |

| (C) Extraordinary Personal Services | §1.469-1T(e)(3)(ii)(C) | Services are so significant that use of property is incidental | Assisted living, medical facilities, boarding schools |

| (D) Customary Rental Period | §1.469-1T(e)(3)(ii)(D) | Rental is incidental to non-rental activity (e.g., property held for investment/sale) | Fix-and-flip investors, developers |

Exception B: Significant Personal Services (The 30-Day Rule)

If your average guest stay is between 8 and 30 days, you can still escape rental classification — but only if you provide "significant personal services" in connection with making the property available. This includes:

- Daily maid/housekeeping service

- Concierge-style services (booking reservations, arranging transportation)

- Providing meals or food service

- Guided tours, entertainment, or recreational activities

This path is less common for typical Airbnb/VRBO hosts, but it can work for mid-term rental operators who offer hotel-like services. Be careful — simply providing linens, Wi-Fi, and a welcome basket does not qualify.

Exception C: Extraordinary Personal Services

Under this exception, the services you provide are so significant that the guest's use of the property itself is incidental to the services received. Think assisted-living facilities, hospital rooms, or boarding schools where the building is secondary to the care being provided. This rarely applies to typical STR investors.

Exception D: Customary Rental Period / Incidental Rental

If the rental of the property is incidental to a nonrental activity — such as a fix-and-flip where the property is rented briefly while waiting for a sale — the rental income is not treated as a rental activity. The rental income must be less than 2% of the property's basis or FMV (whichever is less). This is primarily used by developers and flippers.

For most high-income W-2 earners using Airbnb or VRBO, Exception A (the 7-day rule) is the cleanest and most defensible path. The other exceptions have more subjective tests and are harder to prove in an audit. Stick with 7-day average stays whenever possible.

Test 2: Material Participation

Passing the 7-day test (or any alternative above) reclassifies your property from "rental" to "business." But to claim the losses against your W-2, you must also materially participate in the business. There are seven tests under Treas. Reg. §1.469-5T(a) — you only need to pass one. We cover all seven in the next section.

Material Participation Test #3 (Most Common for STR)

100+

Hours you spend managing the STR

More

Than any single other person

You spend 100+ hours managing the property (booking, communicating with guests, coordinating cleaners and repairs) and no single other person — cleaner, handyman, property manager — spends more hours than you.

Test 3: Cost Segregation

Once you pass Tests 1 and 2, the losses are non-passive. But where do the losses come from? A Cost Segregation Study accelerates depreciation, reclassifying components of the property (appliances, flooring, landscaping, fixtures) into shorter depreciation lives — often qualifying for bonus depreciation.

With 100% bonus depreciation now permanently restored under the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, this creates a massive "paper loss" — typically 20–30% of the purchase price — in Year 1. Because you passed Tests 1 and 2, this entire loss can offset your W-2 income.

It's important to understand how basis works — the cost segregation study reclassifies your basis into shorter-lived asset classes, but it doesn't change your total depreciable basis. If you're not sure whether a study makes sense for your property, our cost segregation flowchart walks you through the decision.

The Cost Segregation Combo: Where the Loss Actually Comes From

The numbers make the case. Without cost segregation, a $500,000 property (excluding land) generates roughly $18,000 per year in straight-line depreciation — a modest deduction spread over 27.5 years. With a cost segregation study, an engineer reclassifies 20–40% of the building into shorter-lived categories:

| Component Class | Normal Life | Cost Seg Life | Examples |

|---|---|---|---|

| 5-year property | 27.5 years | 5 years | Appliances, carpeting, cabinets |

| 7-year property | 27.5 years | 7 years | Furniture, fixtures, equipment |

| 15-year property | 27.5 years | 15 years | Landscaping, driveways, fencing |

Because 5-, 7-, and 15-year property all qualify for 100% bonus depreciation, every dollar reclassified is deductible immediately. On that $500K property with $150K reclassified, that's $150,000 in first-year bonus depreciation alone — plus regular depreciation on the remainder. Timing matters: commission the study in the year of acquisition so the bonus deduction lands in the same tax year as your purchase.

Bonus Depreciation for Short-Term Rentals (OBBBA)

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. The TCJA phase-down schedule (which had reduced bonus to 80% → 60% → 40% → 20%) no longer applies.

Before OBBBA (2024–2025)

40–60%

Reduced bonus under TCJA phase-down

Current Law (OBBBA)

100%

Permanent — no expiration date

What this means for STR investors: A $1.2M property with a cost segregation study can now generate $240K–$360K in Year 1 depreciation deductions — the full amount, applied immediately against your W-2 income. This is the same firepower the strategy had in 2022, but now it's permanent law, not a temporary provision.

Additional OBBBA benefits: The law also permanently extended and increased the Section 199A QBI deduction (up to 23% deduction on qualified business income, increased from 20%) and raised the SALT cap from $10,000 to $40,000. Read our full 100% Bonus Depreciation Guide for details on what qualifies.

The combination of the 7-day rule + Material Participation + Cost Segregation is what makes this the most powerful legal tax strategy available to W-2 earners who invest in real estate. Each piece alone does nothing. Together — especially with 100% bonus depreciation now permanently restored — they can save $100,000–$200,000+ in federal taxes in a single year.

Check Your Eligibility in 5 Minutes

Not sure whether your average stay, hours, and personal use actually qualify? Our free STR loophole calculator walks through the 7-day test, all seven material participation tests, and the questions an auditor would ask — and tells you exactly where you stand.

Run the Eligibility CheckAll 7 Material Participation Tests

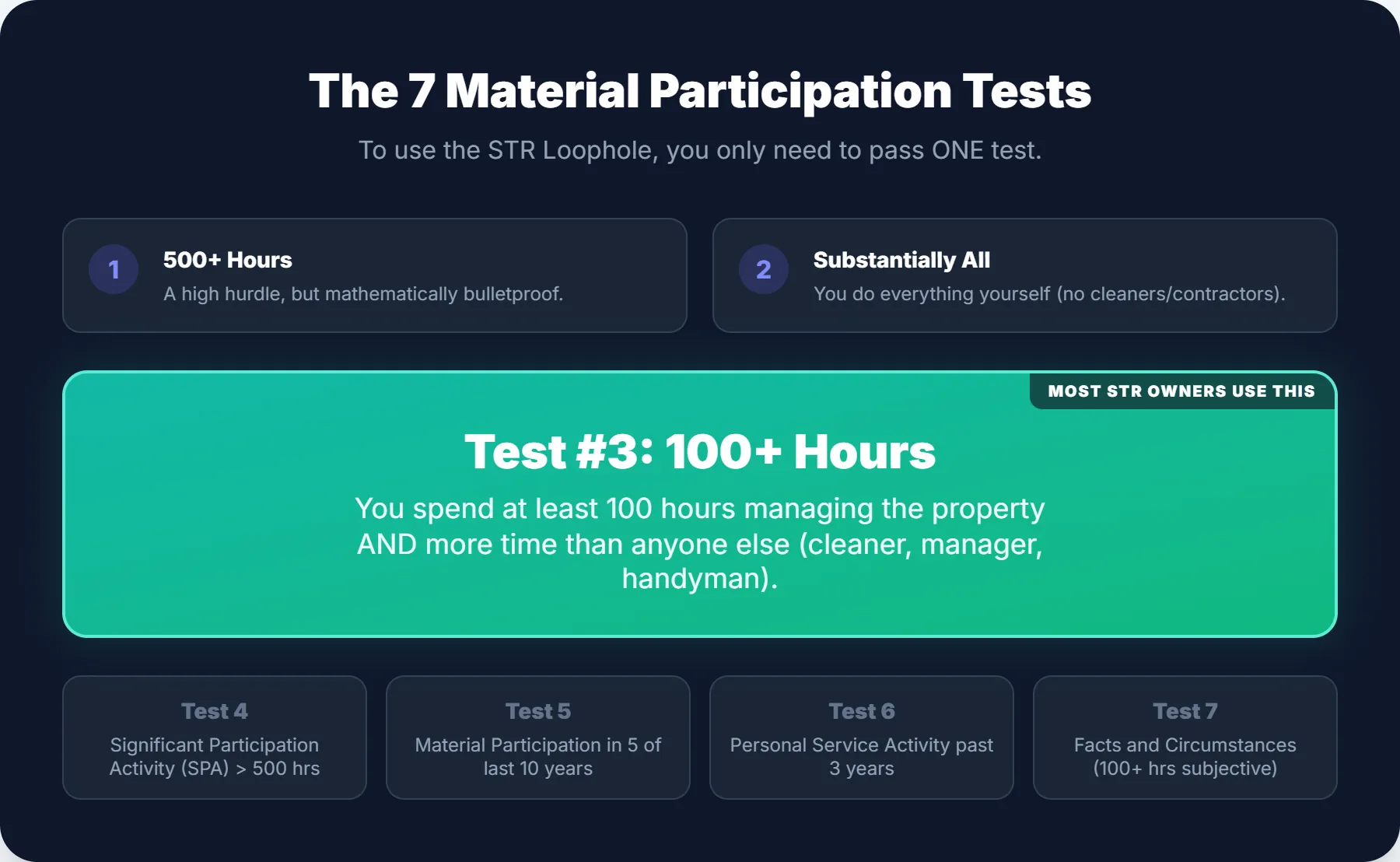

Under Treas. Reg. §1.469-5T(a), there are seven ways to prove Material Participation. You only need to pass one.

Material Participation is where most STR Loophole strategies succeed or fail. Below are all seven tests. For STR investors, Test #3 is the most commonly used, but understanding all seven gives you flexibility and backup options.

Test 1: 500+ Hours

You participate in the activity for more than 500 hours during the tax year. This is overkill for most STR investors — it's nearly 10 hours per week — but it's the most bulletproof test. If you self-manage multiple properties, you may hit this.

Reg. §1.469-5T(a)(1)

Test 2: Substantially All Participation

Your participation constitutes substantially all of the participation in the activity by all individuals (including non-owners) for the year. If you do everything yourself — no cleaner, no handyman, no co-host — you likely pass this test regardless of total hours. However, most STR owners use cleaners, which means another person participates.

Reg. §1.469-5T(a)(2)

Test 3: 100+ Hours, More Than Anyone Else

MOST USED FOR STRYou participate for more than 100 hours during the year, AND no other single individual participates more than you. This is the sweet spot for busy W-2 earners: 100 hours = about 2 hours per week. Just make sure your cleaner doesn't outpace you — if they clean 25 turnovers at 4 hours each (100 hours), you need at least 101.

Reg. §1.469-5T(a)(3)

Test 4: Significant Participation Activities (500+ Combined)

You participate in multiple business activities for more than 100 hours each, and your combined hours across all activities exceed 500. This can work if you own multiple STRs — say 120 hours in Property A, 130 in Property B, and 260 in your consulting business. Combined = 510 hours. Each individual activity must be at least 100 hours to count.

Reg. §1.469-5T(a)(4)

Test 5: Prior-Year Material Participation (5 of 10)

You materially participated in the activity for any 5 of the prior 10 tax years. This rarely applies to new STR investors, but it's valuable if you've been self-managing a property for several years and now want to reduce your involvement.

Reg. §1.469-5T(a)(5)

Test 6: Personal Service Activity (3 Prior Years)

If the activity is a "personal service activity" (health, law, engineering, architecture, etc.) and you materially participated in any 3 prior tax years. This test is essentially irrelevant for STR investing — it applies to professional service businesses.

Reg. §1.469-5T(a)(6)

Test 7: Facts and Circumstances (100+ Hours)

You participate for more than 100 hours and, based on all facts and circumstances, you participate on a "regular, continuous, and substantial" basis. This is the most subjective test and the hardest to defend in an audit. The IRS will scrutinize it heavily. We generally recommend avoiding reliance on Test #7 if possible — Tests #1 or #3 are much safer.

Reg. §1.469-5T(a)(7)

For a single STR property, Test #3 is the path of least resistance: 100+ hours (about 2 hours/week) and more than any single other person. If you own multiple STRs, consider whether Test #4 (combined hours across activities) or Test #1 (500+ total) gives you a better safety margin.

Day in the Life: Material Participation

What 100+ hours of STR management actually looks like for a busy high-income earner.

Friday 6:00 PM — The Inquiry

You just finished work for the day. Your phone pings. A guest named Sarah wants to book your Florida property for 5 days. You accept immediately via the Hospitable app, review her profile, and send a welcome message.

Time Logged: 15 minutes (Communication)

Saturday 10:00 AM — The Turnover

The previous guest checks out. You check your automated lock system. The cleaners arrive. You text them to remind them to refill the propane tank and restock the coffee.

Time Logged: 30 minutes (Supervision/Coordination)

Tuesday 8:00 PM — The Maintenance

The A/C stops working. Sarah messages you. You call your HVAC tech, troubleshoot over FaceTime, approve the repair, and follow up with Sarah to confirm it's resolved.

Time Logged: 2 Hours (Operations)

December 31st — The Count

By year-end, you have logged 112 hours. Your cleaner spent 80 hours. Your HVAC tech spent 4 hours. You have 100+ hours and more than anyone else. You materially participated. The $75,000 depreciation loss is yours to deduct against your W-2.

Tax Result: Non-passive loss secured

The Time Log Is Non-Negotiable

What Activities Count Toward Your Hours?

Not all activity related to your STR counts toward Material Participation. Here's a breakdown:

| Counts ✅ | Does NOT Count ❌ |

|---|---|

| Guest communication (inquiries, booking, check-in/out messages) | Time spent searching for properties to buy |

| Coordinating and supervising cleaners | Driving to/from the property (commute time) |

| Reviewing and responding to guest reviews | Reading articles about STR investing |

| Pricing adjustments (dynamic pricing tools) | Time spent on financing/mortgage applications |

| Furnishing and staging decisions | Passive monitoring (checking an app with no action) |

| Maintenance calls, repair coordination, vendor management | Activities your property manager handles |

| Bookkeeping, tracking income/expenses, paying bills | Investor education courses (unless directly applied) |

| Creating/updating listing photos and descriptions | Time spent on tax preparation (that's your CPA's job) |

| Handling guest emergencies and complaints | Attending real estate meetups (networking) |

Use a simple spreadsheet or app to log your time same-day. Record the date, activity description, and time spent. Courts have consistently sided with taxpayers who maintained contemporaneous logs and against those who reconstructed hours after the fact. We provide our STR clients with a pre-built tracking template.

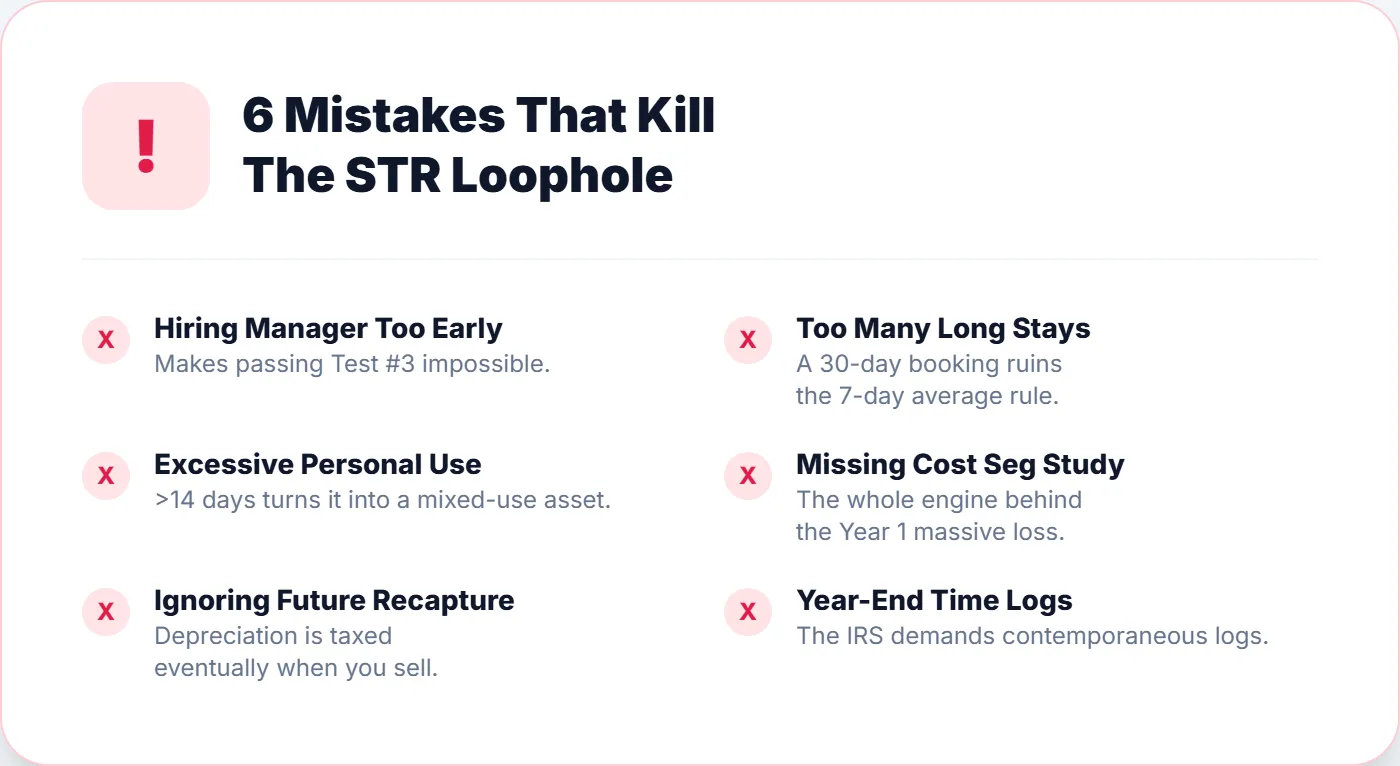

Common Mistakes That Kill the Strategy

We've seen dozens of STR Loophole attempts fail. Here are the mistakes that cost taxpayers the most.

Mistake #1: Hiring a Property Manager Before Meeting MP

If your property manager spends more hours than you on the STR, you fail Test #3. Many investors hire a manager from day one and never log enough personal hours. Solution: Self-manage for at least Year 1 using tools like Hospitable, Guesty, or Airbnb's built-in tools. Bring on a manager in Year 2 only if you can still outpace their hours.

Mistake #2: Accepting Too Many Long-Term Bookings

One or two 30-day bookings can push your average stay above 7 days — especially if you don't have enough shorter bookings to offset them. Solution: Track your running average throughout the year. If you're getting close to 7 days, set minimum/maximum stay requirements on your listing platform to bring it back down.

Mistake #3: Excessive Personal Use

Under IRC §280A, if you use the property for more than the greater of 14 days or 10% of rental days, it becomes a "mixed-use" property. Your deductions are capped at rental income — you cannot create a loss. This completely kills the STR Loophole. Solution: Limit personal use strictly. Maintenance visits count as business days, not personal days, as long as you do actual work.

Mistake #4: Not Getting the Cost Segregation Study

Without cost segregation, your depreciation is spread over 27.5 years — roughly 3.6% per year. That creates a small loss, not the $100K–$300K+ write-off that makes the strategy worthwhile. Solution: Always pair the STR Loophole with a cost segregation study, especially in the year of acquisition when bonus depreciation can be applied.

Mistake #5: Ignoring Depreciation Recapture

When you eventually sell the property, all the depreciation you claimed gets "recaptured" and taxed at up to 25% (§1250 recapture). Many investors are blindsided by this. Solution: Plan your exit strategy from day one. A 1031 exchange can defer the recapture indefinitely by rolling into another investment property. Read our depreciation recapture guide for the full picture.

Mistake #6: Reconstructing Hours at Year-End

The IRS has won multiple Tax Court cases against taxpayers who "estimated" their hours in April for the prior year. A log created after the fact is not contemporaneous, and the IRS knows the difference. Solution: Log your hours weekly, at minimum. Many of our clients use simple Google Sheets with date, task description, and minutes spent.

Mistake #7: Ignoring the Excess Business Loss Limit (§461(l))

Even a perfectly executed STR Loophole loss runs into Section 461(l), which caps how much net business loss can offset non-business income (like W-2 wages) in a single year — roughly $313,000 single / $626,000 married filing jointly (inflation-adjusted). A very large cost segregation deduction can exceed the cap. Solution: The excess isn't lost — it carries forward as a net operating loss — but your CPA should model the cap before you count on the full Year 1 savings, especially on $1M+ properties.

Audit Defense: The Five Records That Win

The IRS knows about the STR Loophole, and audit activity around it is increasing. Your defense doesn't rest on clever arguments — it rests on documentation. Build this file as you go:

- Contemporaneous time log — recorded weekly with date, activity, and time spent. Use a spreadsheet, app, or calendar.

- Rental period records — export your Airbnb/VRBO booking history with check-in/check-out dates, calculate your 7-day average, and keep the math in your files.

- Cost segregation study — from a qualified engineering firm with a property-specific physical inspection, not a cheap "desktop study."

- Guest communication logs — saved exports showing your direct, personal involvement in guest management.

- Contractor records — documentation that cleaners and handymen work under your direction and spend fewer hours than you.

Know the red flags, too: a large Year 1 loss relative to income (expected with cost seg, but it triggers review), a full-service property manager handling everything while you claim material participation, an average rental period suspiciously close to exactly 7 days, and a time log that looks like it was built during the audit.

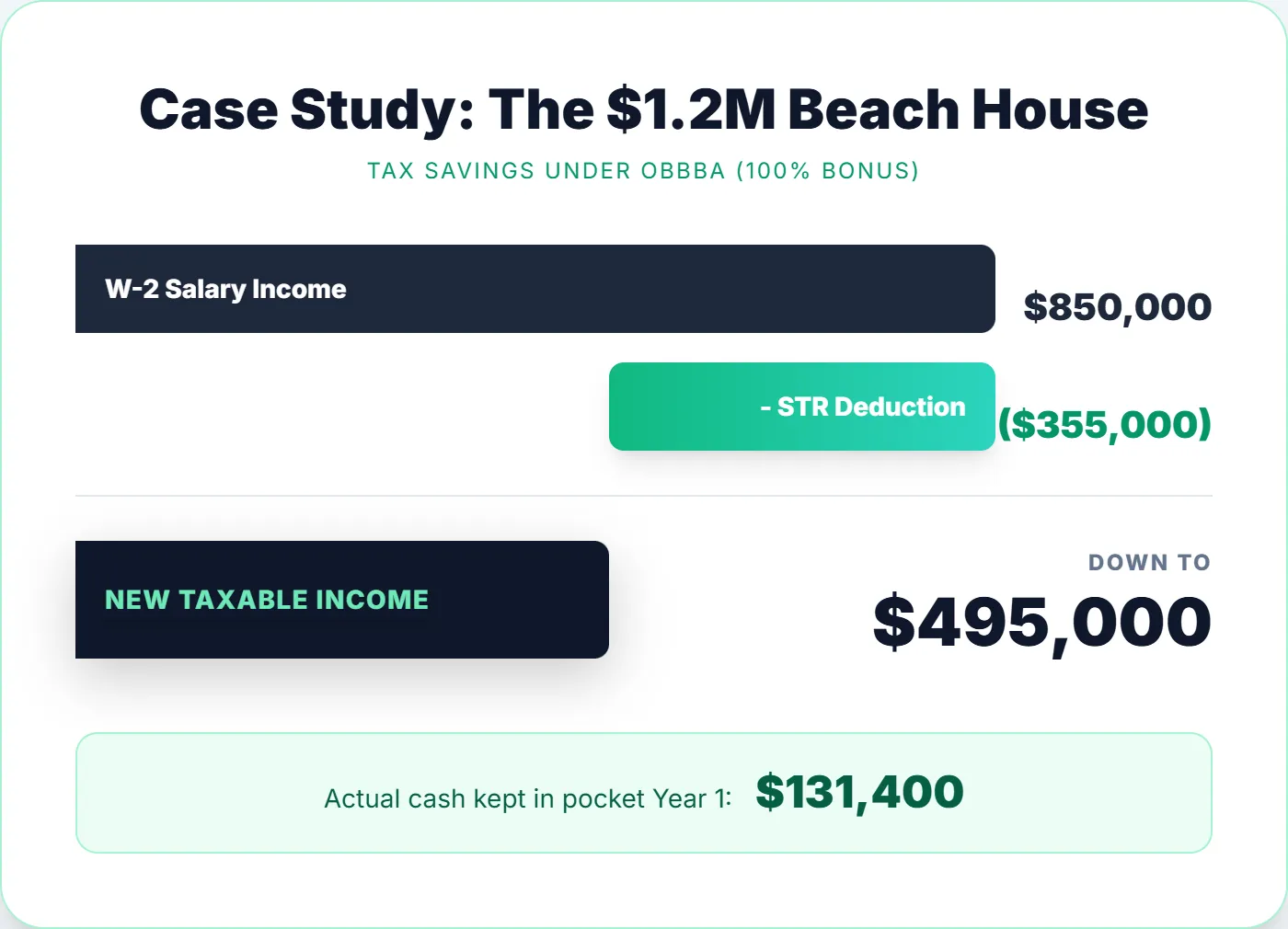

Case Study: The $1.2M Beach House

How a dual-income household saved $131,000+ in combined federal and state taxes in Year 1 under 100% bonus depreciation.

STR Loophole Case Study: $131K Saved in Year 1 (OBBBA Era)

A dual-income household (one spouse in healthcare, the other in tech sales) had a combined W-2 income of $850,000. They were looking at a $280,000 federal tax bill. Under the OBBBA's permanently restored 100% bonus depreciation, here's what happened:

The Purchase

Bought a vacation rental in Florida for $1.2M (80% LTV). Furnished and listed on Airbnb/VRBO.

The Strategy

Self-managed via Airbnb/VRBO to hit 115 hours. Kept average stay under 7 days. Spouse handled guest communication.

The Deduction

Cost Segregation identified $355,000 in accelerated depreciation at 100% bonus (OBBBA). Applied as a non-passive loss against W-2 income.

Tax Savings Summary (100% Bonus Depreciation)

Total Cash Saved in Year 1

$131,400

Combined federal and state cash that stayed in their pocket.

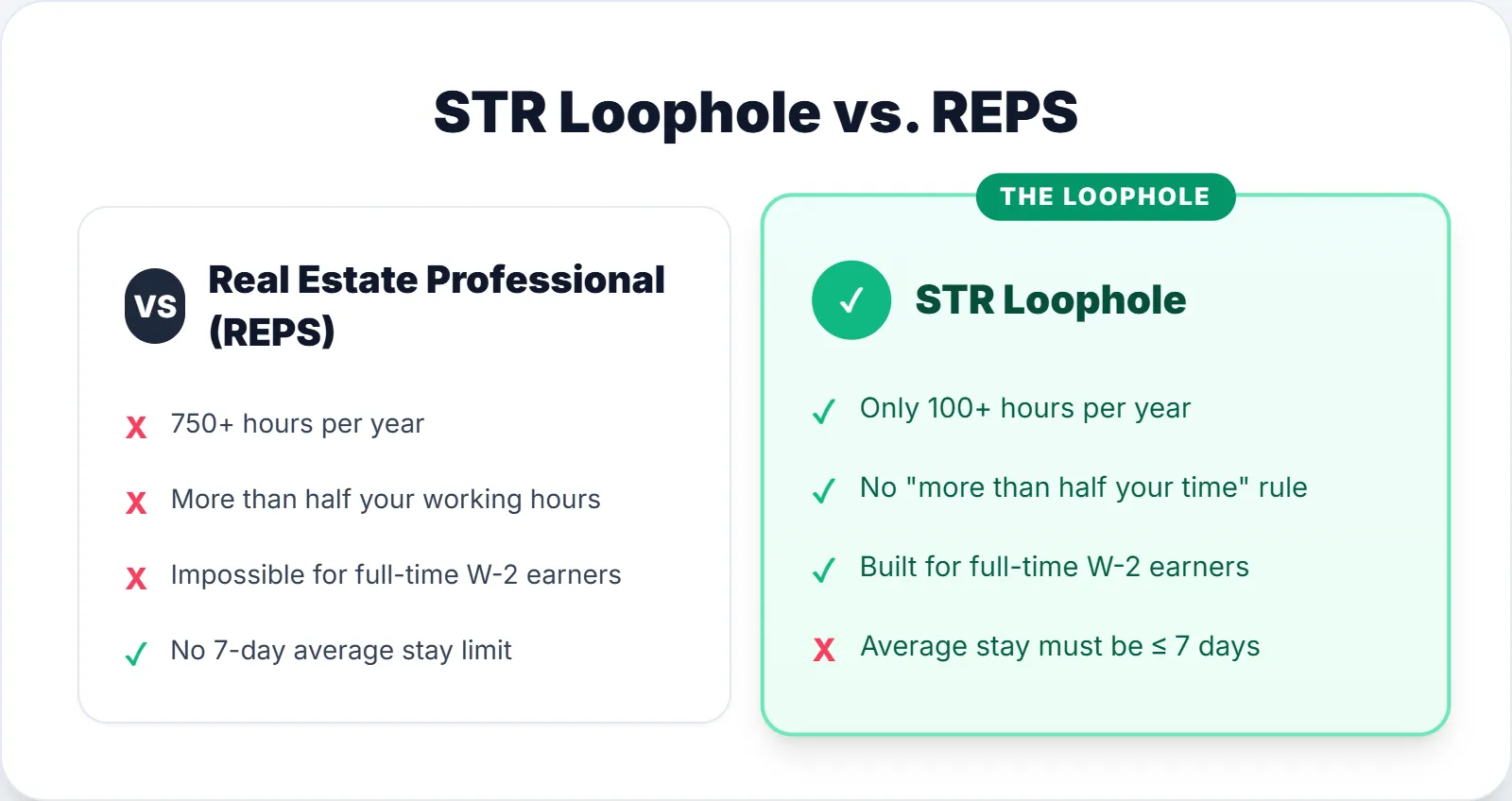

STR Loophole vs. Real Estate Professional Status (REPS)

This is one of the most common comparison questions we get from high-income earners: "Should I use the STR Loophole or REPS?" The answer depends entirely on your work schedule and willingness to manage the property.

Real Estate Professional Status requires 750+ hours per year in real estate activities AND more time in real estate than your primary job. For any W-2 earner working full-time (2,080+ hours/year), REPS is essentially impossible unless your spouse qualifies independently. The STR Loophole, by contrast, only requires 100+ hours — about 2 hours per week — making it the only realistic path for busy high-income W-2 earners who want to offset active income with real estate losses.

If your spouse does not work full-time and is willing to commit 750+ hours to real estate, REPS may be a stronger option because it removes the 7-day average stay requirement entirely. Many of our clients start with the STR Loophole and later transition one spouse to REPS as their portfolio grows.

Section 199A QBI Deduction: An Additional Benefit for STR Owners

The One Big Beautiful Bill Act permanently extended the Section 199A Qualified Business Income (QBI) deduction, which was set to expire after 2025. This is directly relevant to STR Loophole investors:

QBI Deduction on STR Net Income

Because the STR Loophole reclassifies your rental as a business activity, net income can qualify for the Section 199A QBI deduction, reducing your tax rate on that income by up to 23%. This is separate from — and in addition to — cost segregation depreciation.

The QBI deduction phases out for high earners above certain income thresholds ($191,950 single / $383,900 MFJ for 2025). However, even a partial QBI deduction on STR net income can provide meaningful additional savings. Your CPA should model this alongside your cost segregation projections.

SALT Cap Increase: Relevant for High-Income STR Investors

What Is the Airbnb Tax Loophole?

The Airbnb tax loophole is the informal name for the STR Loophole described above. It applies to any short-term rental platform — Airbnb, VRBO, Booking.com, or direct bookings — not just Airbnb. The legal mechanism is identical: under Treas. Reg. §1.469-1T(e)(3)(ii)(A), if your average guest stay is 7 days or fewer, the IRS does not classify the property as a "rental activity." This means the passive activity loss rules of IRC §469 do not apply, and losses can offset your W-2, 1099, or business income directly — provided you materially participate.

The term "Airbnb tax loophole" gained popularity because Airbnb is the largest short-term rental platform, but the tax code does not distinguish between platforms. Whether you list on VRBO, Furnished Finder, or your own website, the same rules apply. The key variables are average stay duration and your hours of involvement — not the booking platform.

How Do You Avoid Tax Problems with Short-Term Rentals?

The most common tax problems with short-term rentals come from three areas: failing to track material participation hours, accepting too many long-term bookings (pushing the average stay above 7 days), and excessive personal use that triggers IRC §280A mixed-use rules.

To avoid these problems:

- Keep a contemporaneous time log — record your STR management activities weekly, with dates, descriptions, and time spent. Courts have rejected reconstructed logs created at year-end.

- Monitor your average stay throughout the year — track total rental nights divided by total bookings. If you're approaching 7 days, set maximum stay limits on your listing.

- Limit personal use — if you exceed 14 days (or 10% of rental days), your deductions are capped at rental income and you cannot generate a loss to offset W-2 income.

- File the correct schedules — non-passive STR losses go on Schedule E with proper elections. Many general CPAs file them as passive by default, costing you the entire deduction.

- Work with a CPA who specializes in STR taxation — the interaction between §469, §280A, and §168(k) bonus depreciation is not something general practitioners handle routinely.

Is the STR Loophole Worth It?

For high-income earners in the 32%–37% federal tax bracket, the STR Loophole is one of the highest-ROI tax strategies available. A physician earning $400K who purchases a $1M short-term rental can generate approximately $200K–$300K in Year 1 depreciation deductions via cost segregation with 100% bonus depreciation (OBBBA). At a 35% marginal rate, that translates to $70K–$105K in real cash savings — in a single year.

The strategy does require work: 100+ hours per year of material participation (about 2 hours per week), contemporaneous documentation, and careful management of average stay duration. You also need to understand that cost segregation accelerates depreciation — it doesn't create new deductions — meaning you'll have less depreciation available in later years, and depreciation recapture applies when you sell (unless you 1031 exchange).

For households earning under $150K, the complexity and compliance burden may outweigh the savings. For households earning $250K+, the math overwhelmingly favors this strategy — especially now that 100% bonus depreciation is permanent under the OBBBA.

Worked Example: $1M STR Purchase — Physician, $400K W-2

Property Details

Taxpayer Profile

Cost Segregation Breakdown

| Asset Class | Recovery Period | Amount | Year 1 Deduction |

|---|---|---|---|

| Personal property (appliances, fixtures, carpet) | 5-year → 100% bonus | $160,000 | $160,000 |

| Land improvements (landscaping, paving, fencing) | 15-year → 100% bonus | $80,000 | $80,000 |

| Remaining building structure | 27.5-year straight-line | $560,000 | $20,364 |

| Total Year 1 Depreciation Deduction | $260,364 | ||

Federal Tax Savings — Year 1

~$91,100

$260,364 deduction × 35% marginal rate = $91,127 in cash kept

State tax savings additional depending on jurisdiction

Physicians: We Built a Dedicated Guide for You

Is There an Income Limit for the STR Loophole?

No — there is no income limit or AGI phase-out for the STR Loophole. This is one of the most misunderstood points in STR taxation, because there is an income limit on the other well-known rental loss break: the $25,000 passive loss allowance under IRC §469(i). That allowance starts phasing out at $100,000 of AGI and disappears completely at $150,000 — which means most high earners get nothing from it.

The STR Loophole works differently. Because a qualifying short-term rental is not a "rental activity" at all under Treas. Reg. §1.469-1T(e)(3)(ii)(A), its losses are non-passive from the start — the passive loss allowance and its phase-out simply never apply. A surgeon earning $700,000 gets the same dollar-for-dollar offset as someone earning $200,000.

In fact, high earners benefit the most: a $260,000 depreciation deduction is worth about $96,000 to someone in the 37% bracket but only about $57,000 to someone in the 22% bracket. The only income-related ceilings to plan around are the §461(l) excess business loss limit (covered in the mistakes section above), which caps how much business loss can offset wages in a single year, and the separate income thresholds on the Section 199A QBI deduction.

Can STR Losses Offset Ordinary Income?

Yes. When your short-term rental passes the 7-day average stay test and you materially participate, its losses are non-passive — and non-passive losses offset ordinary income directly: W-2 wages, 1099 and consulting income, business profits, even bonuses and RSU income taxed as compensation.

Mechanically, the loss is still reported on Schedule E of your Form 1040, but it is not subject to the passive activity loss limitations of IRC §469. It flows through to reduce your adjusted gross income the same year. Contrast that with a typical long-term rental, where the same depreciation loss would be suspended and carried forward — useful only against future passive income or upon sale.

Two practical caveats: the loss must come from a year in which you actually met both tests (qualification is measured every year), and very large losses can bump into the §461(l) excess business loss cap, with the excess carrying forward as a net operating loss rather than vanishing.

What Is the $2,500 Expense Rule for Rental Properties?

The $2,500 de minimis safe harbor (Rev. Proc. 2015-20) allows rental property owners — including STR investors — to immediately expense items costing $2,500 or less per item or invoice instead of capitalizing and depreciating them over multiple years. This applies to tangible property like furniture, appliances, fixtures, and repairs.

For STR investors, this rule is particularly useful for furnishing costs. A $2,200 couch, a $1,800 TV, or a $500 set of linens can each be deducted in full in the year purchased — no depreciation schedule required. The election must be made on your tax return for the year, and it applies to all eligible items, not selectively.

This is separate from — and complementary to — the cost segregation strategy described above. Cost segregation reclassifies building components (flooring, cabinetry, landscaping). The de minimis safe harbor covers movable personal property under $2,500. Together, they maximize your Year 1 deductions from both the structure and its contents.

Important: You Must Make the Election

The de minimis safe harbor is not automatic. You must attach a statement to your tax return electing the safe harbor for each tax year. If your CPA doesn't make this election, you'll be required to capitalize and depreciate these items over their useful lives (typically 5–7 years). Make sure your CPA includes the election statement with your filing.

Is This Strategy Right for You?

The STR Loophole is powerful, but it requires work. It is not a passive investment — it is a business.

Perfect Candidates

Not a Fit If...

Why High-Income Earners Choose Taxstra for STR Strategy

We don't just explain the loophole. We implement it — and make sure it holds up.

The STR Loophole has three points of failure: the 7-day average, Material Participation documentation, and the cost segregation study itself. We manage all three.

- We coordinate the Cost Segregation study — working with qualified engineering firms to maximize your Year 1 depreciation deduction

- We provide Material Participation tracking templates — so you never fall short at year-end

- We model the full tax impact before you buy — projecting Year 1 savings, depreciation recapture, and long-term tax position

- Dual expertise in tax and real estate — our team holds both CPA credentials and a real estate broker license, giving us insight pure accounting firms can't match

- Year-round engagement — quarterly check-ins, mid-year MP verification, and proactive strategy adjustments as your rental business evolves

Featured on The White Coat Investor

Related Strategies

The STR Loophole doesn't exist in a vacuum. Here are complementary strategies our clients often pair with it:

- Cost Segregation Studies — The engine that creates the large Year 1 deduction

- 100% Bonus Depreciation Under the OBBBA — What qualifies and how to maximize your Year 1 deduction

- STR Loophole for Physicians — Physician-specific guidance for hospital W-2 and locum tenens income

- Real Estate Professional Status — An alternative path if your spouse can qualify

- Depreciation Recapture — Understand what happens when you sell

- Entity Structure — Whether to hold your STR in an LLC, S-Corp, or individually

- Solo 401(k) — Retirement savings if your STR generates self-employment income

Authoritative Sources

- Treas. Reg. §1.469-1T(e)(3) — Definition of rental activity (7-day rule)

- IRC §469 — Passive activity losses and credits limited

- Reg. §1.469-5T — Material participation tests

- IRC §168(k) — Bonus depreciation (100% under OBBBA)

- IRC §280A — Personal-use limits on dwelling units

- IRS Audit Technique Guide — Passive Activity Loss

Citations reflect U.S. federal tax law as of the article's last reviewed date.

Frequently Asked Questions

Still Researching? Get a Personalized STR Tax Savings Estimate

Tell us your purchase price and household income — we'll send back a projected Year 1 deduction estimate within 24 hours. No call required.

Every Year You Wait Is a Year of Taxes You Didn't Have to Pay.

The STR Loophole is a 'use it or lose it' opportunity. We specialize in short-term rental tax strategy for physicians, tech professionals, and high-income W-2 earners. Let's see what's possible.

Book a Free ConsultationNo obligation • Takes 30 minutes • Done over the phone

About the Author

Bryan Martin, CPA • Licensed Real Estate Broker

Bryan is the founder of Taxstra PLLC, a CPA firm specializing in tax strategy for high-income earners, real estate investors, and business owners. He holds both a CPA license and a real estate broker license, giving him a unique dual perspective on real estate tax strategy. Bryan was featured on The White Coat Investor Podcast (Episode #459) and works with clients nationwide from his base in Springfield, IL.

Learn more about Bryan →